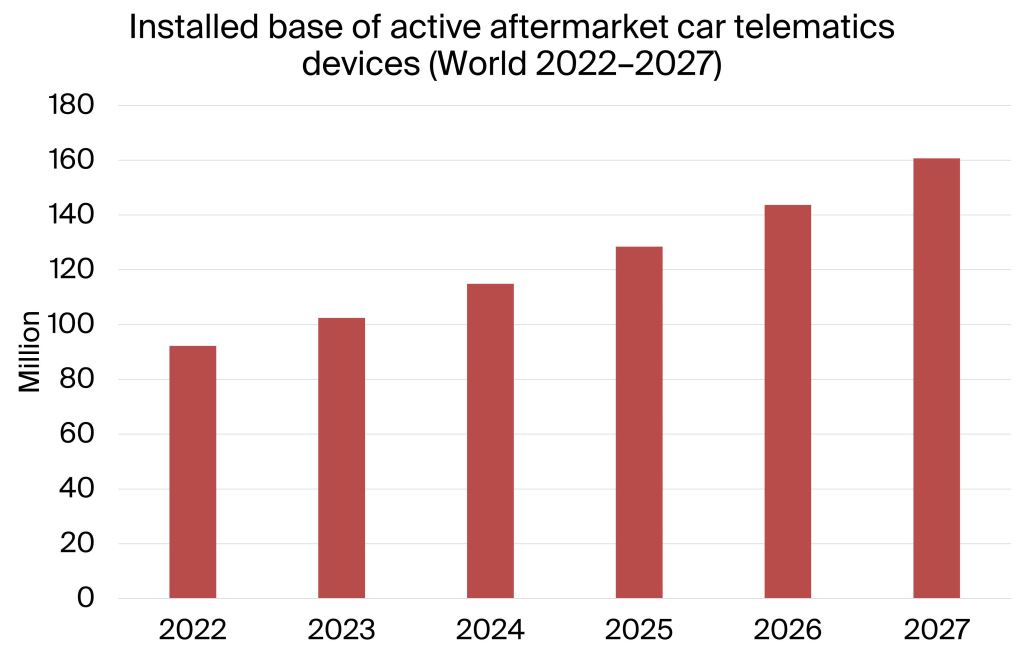

Gothenburg, Sweden – July 21, 2023: According to a new research report from the IoT analyst firm Berg Insight, the number of active aftermarket car telematics units will grow at a compound annual growth rate (CAGR) of 11.7 percent from 92.2 million at the end of 2022 to 160.7 million worldwide at the end of 2027. Berg Insight’s definition of an aftermarket car telematics solution in this report comprises both cellular/GNSS and RF-based solutions. Aftermarket car telematics solutions are useful in a number of application areas including stolen vehicle tracking and recovery (SVT/SVR), vehicle diagnostics, Wi-Fi hotspot, convenience applications and usage-based insurance. Vehicle diagnostics allow service providers such as dealers and workshops to improve service offerings to car owners. Dealers and finance companies can moreover leverage telematics for internal fleet management and manage the customer lifetime value. Aftermarket car telematics services are offered by a wide range of players.

“Examples of leading telematics companies selling services via third parties or directly to consumers include Octo Telematics, Spireon, Procon Analytics, StarLine, Targa Telematics, Vodafone Automotive, Ituran, Tracker Connect, SareKon, PassTime GPS, iMetrik, Mojio, CalAmp (LoJack), Verizon and Viasat Group”, said Martin Cederqvist, IoT Analyst at Berg Insight.

Distributing services and products through third parties is the most common go-to-market strategy for aftermarket car telematics solution vendors. Important sales channels include insurance companies, dealers and importers as well as direct-to-consumer channels such as mobile operators and online retailers. Aftermarket services targeting a specific customer group can furthermore gain an advantage in specialisation compared to OEM telematics services that are developed for a wide range of use cases. Dealers is an example of a customer group that aftermarket service providers serve successfully as the telematics offering can be adjusted to fit their business needs.

“Even though OEM telematics systems are becoming more common, many dealers are interested in aftermarket telematics systems for customer management as well as lot management. Aftermarket car telematics hardware enables dealers to access data in an actionable format across car brands and trim levels. Telematics service providers close the gap between automotive OEMs and dealers by aggregating data and providing actionable insights.” continued Mr. Cederqvist.

Regional market conditions such as a high level of vehicle crime influence the demand for stolen vehicle tracking and have made SVT solutions popular in countries such as Brazil, Argentina, China, Israel, Russia and South Africa. “The number of dedicated active aftermarket SVT units in use is forecasted to reach 88.7 million in 2027, up from 55.1 million at year-end 2022”, said Mr. Cederqvist. Today, there are many different form factors applicable for aftermarket car telematics ranging from professionally installed hardwired blackboxes to self-installed OBD dongles and battery-powered devices. Solutions aimed at dealers and vehicle finance institutions in the US mainly use LTE -M devices and LoRaWAN has become a connectivity option for asset tracking and SVR in Latin America, North America and Europe.

“Albeit aftermarket car telematics services face competition from smartphone-only and OEM solutions, it still has a dominant position on the market in many parts of the world. Even in markets with high adoption rates of OEM telematics services, aftermarket telematics services are expected to be increasingly popular in the coming years”, concluded Mr. Cederqvist.

Download report brochure: https://media.berginsight.com/2023/07/21234107/bi-aftermarketcar4-ps.pdf