At an insidious level, there are far reaching changes taking place in the ways vehicles and their components will be built in the future. A software-defined vehicle concept is quickly becoming a reality. Cars and trucks generate enormous amounts of vehicle and driver behavioural data daily. This data is valuable to carmakers and suppliers, as well as to content and service providers including dealers, fleet operators, insurance companies, retailers, and gas stations. However, before this valuable data can be analyzed or even monetized, it needs to be harvested from the vehicle. This is going to require massive changes in the way vehicle design is conceptualised. Vehicle manufacturers and OEMs are building a secure and reliable vehicle-to-cloud data exchange platform not only to collect the vehicle data but to facilitate software updates and deliver content. Most importantly, all the players in the value chain need to take cognizance of the fact that the data generated can provide a valuable income stream.

Ultimately, high-tech companies, start-ups, alternative mobility operators, data management services, insurers, roadside assistance providers, and infrastructure operators will all be players in the car data monetization landscape. However, it is the most traditional of automotive players, who may find staking a claim most challenging. OEMs and suppliers are accustomed to seven-year product cycles, full control over a stable value chain, consolidated monetization models, and few interactions with end customers. They are also used to delivering products and services with limited digital capabilities. Car data monetization will challenge

all of these current realities and compel them to undergo a sea change in their entire thinking process. Besides hugely enhanced IT and data analytical services, it will also require a shift from being pure product company to service providers who interact with the end consumers and integrate changes in their products based on feedback.

For traditional players like automobile OEMs or tier-1 suppliers, building and operating service businesses is a new and significant challenge, requiring the development of specific capabilities either internally by developing digital talent or externally by partnering with or existing players in the field. From a skill set point of view in order to monetize any car data some basic data management capabilities are required:

- Collection, cleansing and formatting of data from a multitude of relevant sources – the car, OEM Web site, social media and the dealer management system

- Data analysis that applies “big data/advanced analytics” techniques to extract valuable insights from this wide and complex data landscape

- Generating insights, which will ultimately result in deploying features, products, services, and recommendations to customers and/or to business partners to complement the offering and refine them to ensure that the highest levels of customer satisfaction are achieved.

However, this shift in an extremely traditional industry is not easy. Pushing beyond the basics, making services, R&D, factories, and channels digital ready, especially for traditional automotive organizations – is resulting in a fundamental paradigm shift in the automotive sector. Industry executives concur that organizational complexity and a lack of specific digital skills fundamentally can still delay OEMs’ ability to innovate at the rate of nimbler high-tech players and start-ups.

Besides changes within the organisation, technology, market, and regulatory trends will also make strategic collaboration increasingly necessary. Openness and agility in creating partnerships in R&D and sales channels development will be required to succeed. We are witnessing therefore an enormous mind set change in the automotive industry, in what used to be an extremely traditional, closed ecosystem.

However, path breaking as these changes may seem, there has already been some progress made in the field. A multitude of use cases already exist in today’s market. Connected car services such as remote diagnostics, remote vehicle control, eCall, Bcall and Real-time traffic monitoring have already seen increasing adoption of trends among the consumers. And going forward, with the advent of 5G technology in the automotive ecosystem, a further increase in adoption rates of other potential use cases as well as, V2X, UBI and in-car commerce can be expected to accelerate.

According to an Intel study smart vehicles will produce 4TB of data for every 1.5 hours on the road. With that volume of data, the next challenge for automakers will be how much information is openly available to third parties while also securing the system from misuse. One emerging strategy takes some of the heavy-lifting off the telematics control unit (TCU) by processing only real-time needs locally and passing subsets of data to the cloud. More complex AI and analytics can unburden the TCU by making use of ultra-low latency Network Edge Compute technologies.

There are a number of ways to monetize vehicle data. The two main categories are of course cost savings and new revenue generation. OTA software updates and early recall management can save automakers millions of dollars. Real-time data feeds will also help their R&D efforts tremendously. Interestingly, although cars have been equipped with some tools of data mining, two wheelers remain largely untapped. Two-wheeler users will definitely benefit from their riding behaviour analysis and custom UBI offers. Thus, while modern cars come with factory-installed TCUs, this is not the case for motorcycles, scooters, ATVs and other powersports vehicles. Only recently, the leading powersports OEMs have started equipping their flagship models with TCUs.

The ability to monetize car data hinges on the technological development and customer acceptance of in-car technology and the interconnections of the various data sources and data management tools. For instance:

Vehicle technical sensors monitor the vehicle’s performance status, track malfunctions, and enable remote/predictive maintenance capabilities. Moreover, collecting data on running cars allows OEMs and suppliers to observe how their products withstand usage and establish a clear cause-effect relationship for breakdowns. However, setting the type and frequency of data gathering and integrating the findings with R&D processes represents a challenge that OEMs and suppliers are still tackling.

Environment sensors detect data related to whatever is around the car. For instance, the road, weather, nearby vehicles and other hazards as well as inside the car – the driver, passengers, and the cargo. For instance, a set of sensors could be fitted to monitor the driver’s physical condition vide his vital signs (e.g., heart rate, blood pressure) or even his sobriety. Monetization opportunities here will largely depend on the degree to which customers are willing to share bio-information about themselves and their passengers.

HMI and customer ID. The HMI is the set of technologies by which end customers access and activate the vehicle’s features and receive the outputs of the vehicle’s computing system in response. Buttons, touch screens, voice commands, and visual or gesture recognition sensors are among the technologies that must be reimagined to create an optimal user experience.

Connectivity concerns the link between the vehicle, its onboard sensors and devices, and the Internet. The gateways of connectivity include Wi-Fi, Bluetooth, USB, RFID, and radio. However, it is perhaps the high-speed 4G/5G modem gateway that comes with the biggest challenges. As vehicles travel, geographical gaps in high-speed data connectivity become an issue that must be resolved, along with the significant cost of continuousdata connectivity.

Onboard data storage is the local hardware repository for data generated by the vehicle. Necessary developments in this area include determining which data is stored onboard and who has access to it (e.g., insurers) as well as ensuring that this data is protected.

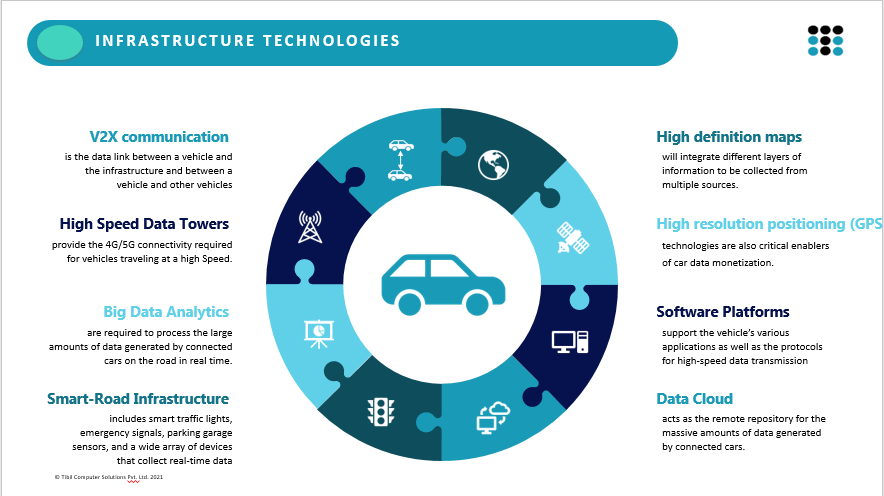

Beyond the processors, sensors, and gateways with which the vehicle itself is equipped lies a network of external technologies that are linked to the road itself or related to the operation of the in-car technologies. The development of these infrastructure technologies are fundamental to car data monetization.

High-speed data towers. An adequate coverage is the key to maintaining continuous and reliable performance. The deployment speed and cost of the towers are central issues. For this reason, an array of alternative connectivity technologies (e.g., satellite based) are being explored for low-density areas.

V2X communication. The successful transmission of traffic, safety, and social data may depend, in large measure, on the development of standard formats and frequencies that facilitate this communication. The standardization of communication protocols represents an ongoing challenge for industry players, even more so considering the safety-critical communications for autonomous vehicles.

Smart-road infrastructure. One of the biggest challenges as costs to fit the road system are likely to be significant and hence multiple questions about financing the investment by cash-strapped governments and municipalities have yet to be fully answered.

Big data analytics. While Industry players are already developing internal competences in advanced analytics that will enable them to leverage this strategic asset, a lot of heavy lifting will still need to be done by tech companies and tech start-ups to bridge the gap.

Data cloud. The required capacity and redundancy, security levels, and access rights are often the critical elements to be determined.

High-definition maps. Highly accurate 3D map used in autonomous driving, containing details not normally present on traditional maps. Such maps can be precise at a centimetre level. HD maps are captured using an array of sensors, such as LiDARs, radars, digital cameras and GPS.

Software platforms Questions regarding the reliability of OTA software updates and which of them consumers will pay for are fundamental to successful car data monetization.

Location/navigation. Which map’s “technical archetype” to adopt, how maps are updated, and how vehicle location (i.e., GPS) information is stored, shared, and transmitted are among the critical decisions going forward for industry players.

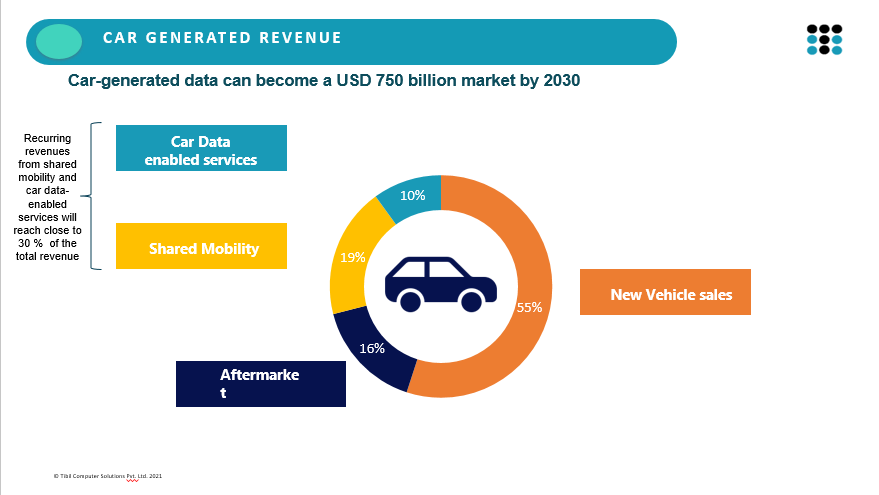

With the increasing proliferation of new features and services, car data will become a key theme on the automotive industry agenda and – if its potential is fully realized – highly monetizable. It is estimated that by 2030 a total revenue of 750 billion by 2030 can be generated by data enabled services.

What this means is that this will lead to an unprecedented explosion in car-generated digital data, with significant implications not just for the traditional automotive industry businesses but also for new players. Companies representing high-tech, insurance, telecommunications, and other sectors that at once seemed, at most, “automotive adjacent” will play critical roles in enabling car data-related services and monetize the same.

Author:

Markus Pfefferer

Managing Partner

TIBIL Computer Solutions Pvt. Ltd

Mr. Pfefferer, Managing Partner at Tibil Solutions has particular expertise in global strategic planning throughout several industries including technology, renewable energy, automotive, heavy engineering. Specializing in market development and implementation of business plans, product development, and management of international business development; Mr. Pfefferer has been influential when partnering with clients in establishing business strategies throughout Europe, Middle East and Asia Pacific.

Published in Telematics Wire