The last two decades have seen rapid urbanization led change in lifestyle in Indian cities, with private vehicle ownership being a requisite status symbol. Rising incomes and lack of public transport kept putting more private vehicles on the roads with cities such as Bengaluru, New Delhi, and Mumbai now among the top 10 most congested cities in the world.

Congested roads, long daily travels, and low vehicles per head, amidst rising disposable income and smartphone penetration make for a perfect recipe for shared mobility uptake – catching the eye (and billions of dollars) of global shared mobility investors.

Few years back Uber and Ola emerged on our smartphones and changed the rules of mobility. The millennials took an immediate liking to it, of course those ‘free rides’ and deep discounts were the catalyst (bargain hunting is a constant among Indian generations!) – a viable alternative to private vehicle ownership was born.

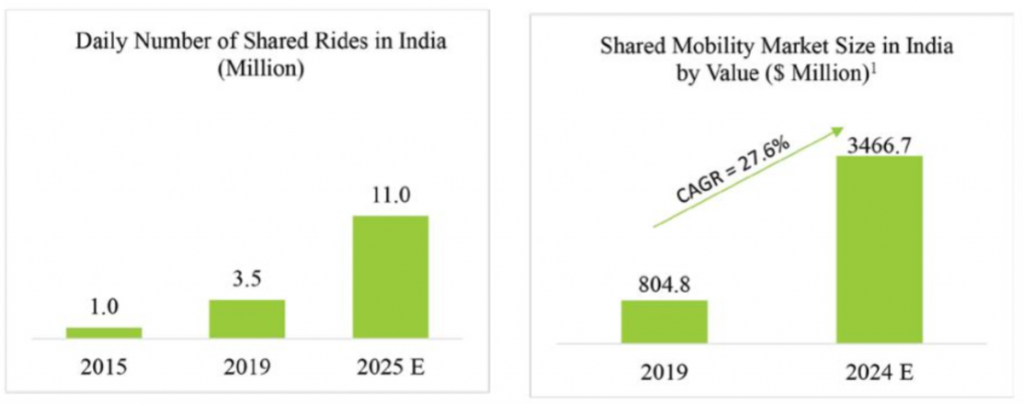

So how strong is this demand for shared mobility?

According to a Morgan Stanley report, by 2030, 1 in every 3 miles travelled on Indian roads will be via shared mobility, rising by more than three-fold vs. the current levels.

A survey by McKinsey showcased that 78% Indians (vs. 53% global average) were willing to give up their private car for cost effective shared mobility.

Moreover, millennials around the world have showcased an increasing preference for shared mobility vs. private vehicles, a trend that is likely to be magnified in India with its 400 million millennials (half of country’s active workforce).

This high growth potential has led foreign investors to place their big bets for APAC’s shared mobility on India, particularly after China proved to be a tough nut to crack for them.

Are Factors Driving the Indian Shared Mobility Distinct?

The sharp uptake of shared mobility has been global, however, the demand drivers and challenges in Asian countries such as India are pretty distinct vs. the Western world, we have a look at some below:

| Factor | US and EU | India | Details |

| Price Sensitivity | Medium | High | Demand for mobility in India is highly price elastic, Shuttl’s success has showcased that riders are accepting of waiting time and point pick-up and drop if the service is priced lower |

| Reliance or Scope for Micromobility | Low | Very High | Two-thirds of all work-related trips in India are short (<5km) – an ideal distance for Micromobility – unlike Western countries, use of 2-wheelers is widespread in India, with low upfront investment and short payback period making it a potential growth juggernaut |

| Customized Solutions for Each City | Medium | High | Language, terrain, road network, and public transport vary significantly across Indian cities – calling for highly customized mobility solutions – for example, New Delhi’s extensive metro network is ripe for uptake of point-to-point services such as Yulu; European cities typically have several common features (such as strong local rail network) |

| OEMs Active in Shared Mobility | High | Low | Unlike Europe and US wherein OEMs have poured billions into shared mobility, India’s leading OEMs have been coy, barring an odd deal between Hyundai–Ola and Maruti Suzuki’s small investment in setting up a R&D unit for this space |

| Role of EVs and AVs | Very High | Low | The developed countries have been gung-ho about how EVs and robotaxis will give shared mobility the cost advantage vs. private cars, however, India’s inadequate infrastructure and investment in EV and abundant manpower make these two phenomena less irrelevant, at least in the medium term |

| Uniform Govt. Policy and Support | Medium | Low | As many European and South-east Asian cities are working with various private stakeholders including mobility players to develop Smart Cities, the Indian government has been muted in providing policy or funding to support shared mobility uptake – on the contrary, many Indian cities have cited ride hailing and related services as ‘illegal’, bowing to the pressure of the strong local taxi unions |

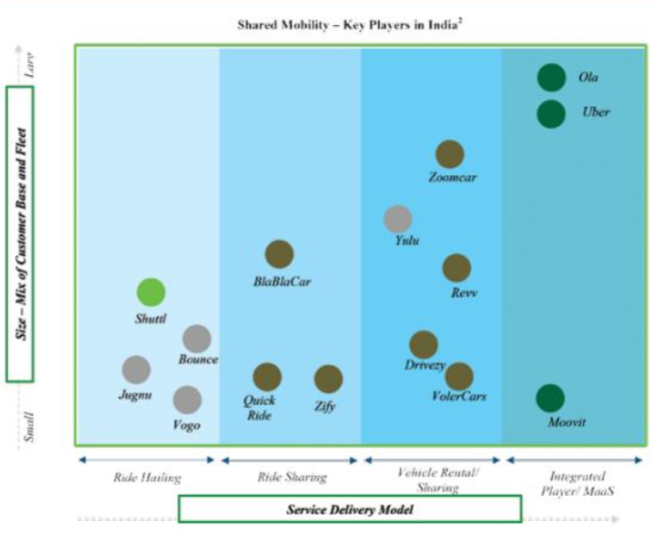

Players Adopting Varied Business Models and Offerings, Who Will Win?

Once Ola and Uber established a large active consumer base for app-based shared mobility, many specialist/niche players have started emerging in this space over the past couple of years.

Now, with PE investors putting a plug on cash burns, deep discounts have become a thing of the past with shared mobility players in India trying to gain the competitive edge by either serving the right niche or expanding operations to become a one-stop-shop.

No deep discounts anymore! – so what’s the plan?

Large players such as Ola and Uber control lion’s share of the market and are now moving towards positioning themselves as MaaS providers, whilst specialist players such as Yulu are looking to carve out a small market for themselves, serving just the first or last mile of the journey.

Moreover, Ola and Uber are now channelizing their funds to move from passenger travel to delivering goods as well, with a view to create an integrated mobility platform. Some recent reports suggest that car-based ride hailing’s new demand has been flattening lately; investors keenness to invest in emerging mobility segments such as Micromobility also suggests that stakeholders are looking at new avenues for exponential growth.

About the Author:

Rajat Gupta

Manager, The Smart Cube

Shared Mobility | 5G | AV/EVs

Helping clients across the globe find answers and opportunities in the fast-changing location intelligence, shared economy, automotive, and 5G technology space.

Published in Telematics Wire