Due to all the good reasons, pay-per-use is all the hype right now. Whether it’s cloud tech, software solutions, electricity, mobility and even water. Consumers are adept to pay per use for most physical goods and now services are also being packaged to accommodate that pricing.

That being said, it’s in no way an easy feat to achieve. Thankfully, we now have disruptive technologies and adaptive consumers making it easier for companies to introduce mind-boggling concepts. One of these crazy ideas was to charge insurance premiums based on your driving behaviour. So next time you overspeed, you may end up with a speeding ticket along with a higher premium for insurance. This will be a real-time analysis of your driving behaviour with an immediate effect on usage-based insurance, Usage-based Insurance (UBI). On the other hand, if you are a good driver, you may get a real-time discount on your car insurance.

The global Usage-Based Insurance Market size stood at USD 19.6 billion in 2021 which is projected to reach USD 66.8 billion by 2026. That means growing at a CAGR of 27.7%.

The Mechanics Making It Possible

Since Usage Based Insurance (UBI or telematics) relies on driving data it is important to understand what, how and why data collection, analysis, and insights for computing your vehicle’s insurance. The more data points a system can gather, the more efficiently it will understand the driver’s behaviour and efficiency. Thus, creating an effective reward-based model. A typical UBI insurer collects the below data:

- Miles driven

- Time of day

- Speed

- Acceleration

- Hard cornering

- Hard braking

- Accidents

- Phone use while driving

All these data points have their own value in the UBI equation. For instance, speed, hard acceleration, hard breaks, cornering etc. indicate responsibility while miles driven, and stops indicate usage load. Through these factors a system can also detect sudden changes in driver’s behaviour indicating intoxication or use of vehicle by multiple drivers.

Now that we understand what needs to be tracked let’s see how we can track these data points. While some cars have in-built capabilities like BMW ConnectedDrive or OnStar, any car can be easily tracked using an external data aggregator. We can plug an IoT device in the car’s onboard diagnostics (OBD-II) port or simply use a smartphone app all like Allstate Drivewise, BytEdge’s SmartDrive or Farmer’s Signal. Some companies also use a tag device that can be attached to the windshield or rear window and pairs with your smartphone via Bluetooth. For example, Liberty Mutual Insurance RightTrack. This further enhances the smartphone’s capabilities to gather required data.

The choice of data collected, and the technology used depends in the usage-based model a company wants to use. Below are some of the prominent ones:

- Pay as You Drive (PAYD): Charging based on distance travelled

- Pay How You Drive (PHYD): Evaluating driving behaviour like acceleration, braking, etc. to determine premium amount

- Pay as You Go (PAYG): Using telematics devices and/or phones to understand both distance and driving behaviour.

The choice of model depends on the technical capabilities of the company, user’s consent, and ease of market penetration. For instance, in the US, it is easier to find cars that already have a data collection mechanism but the same won’t hold true for Georgia or Belarus.

It’s more than what meets the eye!

The subtle thing behind UBI is that it’s not just about insurance. The world today is a big narration of a story where data is the protagonist. UBI gives a simple yet powerful excuse to insurance companies to get their hands dirty in the stream so profoundly leveraged by the big apple, jolly good fellows and the blue screen of death. Here are some of the many advantages of telematics (UBI) car insurance:

- Drivers can learn about their habits and how to ensure their on-road safety.

- The idea of lower premiums can encourage people to drive cautiously, limit phone use while driving and adhere to speed limits.

- Identifying potentially intoxicated driver can help authorities limit accidents by being proactive instead of reactive.

- It helps in exercising parental control which can even boost sales of cars for younger drivers

- Businesses involved in commercial use of vehicles can assess driver’s performance and even reward good drivers.

- Eliminate non-driving factors in car insurance rates, such as credit score, income, occupation, education, etc.

- Insurance companies can create attractive offers and improved need-based insurance policies for specific car owners.

What other possibilities vehicle data might open is only limited by our imagination. One wild thought can be to use the behaviour data of good drivers to refine self-driving programs. Keeping speculation aside, even the direct benefits are too good to be left uncapitalized.

Why it isn’t mainstream already?

With so many advantages in favor we ought to ask ourselves as to why this technology is not synonyms with buying a car. Surely the insurance and automobile giants have enough resources to make it happen. Well, as with any other technology, Usage Based Insurance suffers from its own complications.

Privacy and Security Concerns:

Some drivers are uncomfortable with their data being shared for the sake of insurance. It’s even possible to misuse this data as one can easily know about a person’s whereabouts if the PII guidelines are not taken care of. In the 2021 Telematics Consumer Survey conducted by Arity, 35% of respondents shared their concerns about how driving data is used or shared and 34% of respondents were also concerned about whether a fair assessment criterion will be deployed.

Need for Transparency:

We can’t all be happy with an algorithm telling us we are bad drivers! Consumers demand openness in such cases to self-check whether they are treated fairly or not. The Consumer Federation of America (CFA) holds the view that telematics could even end the use of non-driving factors while deciding premiums, but it hasn’t seen regulators doing their part of removing discriminatory fields from the forms.

In a recently published white paper, the CFA says that telematics programs currently lack rules for pricing transparency and consumer privacy. The organization says that telematics could help insurers end the use of non-driving factors in pricing, but regulators must make sure that UBI programs don’t create new forms of unfair discrimination in auto insurance. The CFA is suggesting that state regulators take certain steps like the below to promote fair use of UBI:

- Make it mandatory for insurers to showcase the actuarial basis for the data that’s collected and analyzed.

- Ensure consumer consent is taken explicitly for use of data.

- Prohibit any exchange of telematics data for non-insurance purposes.

- Require insurance companies to test minimize any negative impacts on protected classes (based on race and ethnicity).

- Consumers should have the option to review their telematics data and use it for claims settlement

- Tech companies working on telematics algorithms should be licensed as insurance advisory organizations thus, making them subject to state insurance regulations.

Even though this is for the US based consumer we can expect the same expectations and guidelines for companies across the world very soon.

Product Pricing:

It’ll be difficult to convince customers to invest in data collection hardware or even sign up for the scheme unless considerable discount is offered on the premiums (i.e., at least from 10% to 15%).

As per LexisNexis 2013 Insurance Telematics Study, 72% of drivers are more willing to opt or telematics solutions if they get at least a 10% discount for the first 6 months.

This means the first movers in the market will have to invest in hardware and offer discounts and those who enter after-market maturity can still maintain their share without investing heavily in marketing, discounting and hardware at the same rate.

A hope for a better tomorrow

All said and done, we can be positive about the future of UBI. An ever-increasing need for greater connectivity and intelligence in vehicles coupled with the rise of connected cars means that soon we can even stop considering hardware as a limitation. Moreover, insurance companies can alert authorities in case of emergencies like accidents or brake failures. Hence, there is an increasing willingness of governments to mandate such services in the interest of road safety, which is already happening in the European Union and Russia.

While the insurance big daddies have strong global distribution networks the new age startups have flexibility and core tech expertise on their side. Maybe we are eventually moving to a fairer competition in insurance as well.

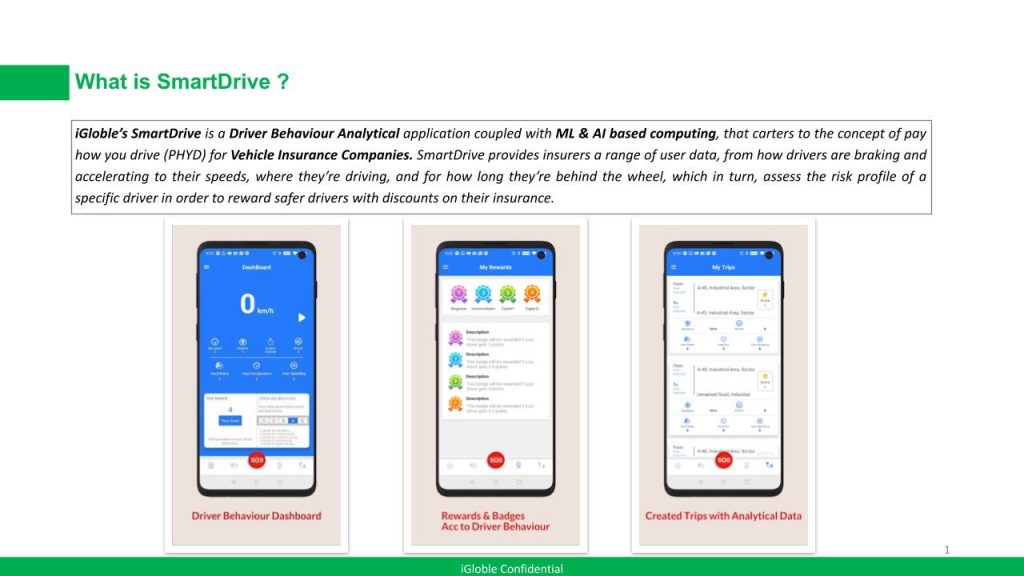

At BytEdge, we have created SmartDrive to help insurers collect all the necessary data for Usage Based Insurance schemes. The app doesn’t rely on any external device like an RFID tag hence, it significantly reduces the technical challenges and costs involved in the process.

As we can see in the screenshot above, through a mobile app user can share driving related data with the insurance companies, access past data and enjoy rewards for good driving behavior. This effectively gamifies the whole process keeping users engaged with the app and the company.

Author:

DR. AMIT SHEKHAR

Founder & CEO

BytEdge, Inc.

He is a Visionary IT Transformation Leader with over 20 years of experience to transform organizations to achieve competitive advantage and efficient operations. He has significant experience in consumer/retail, manufacturing, high tech, and automotive domains. He has worked with – Procter & Gamble, General Electric, Xerox, Caterpillar, Anheuser Busch, Best Buy, Smuckers, Texas Instruments, HP, and many more.

Published in Telematics Wire