Aftermarket telematics, as its name suggest is a Telematics Solution which gets retrofitted by the Vehicle Owner primly for vehicle tracking, fuel monitoring, driver monitoring etc. Hence its done purely based on an actual need and not just a feature coming fitted in a vehicle.

The Aftermarket telematics got its significance in the early 2000s when Big Fleet companies, large Oil and Mining Corporations made it mandatory to track their vehicles. Earlier, it was just to ensure the security of passengers as well as checking speed limits in big campuses and oil fields. Later, the product evolved and were tailor made according to the variety of requirements of individual customers and industries. This paved the way for much wider penetration of the product into smaller Fleets.

The evolution of industry has been so rapid that the quantum of data captured from vehicles has changed from simple locations and speed to the minute of its detail including engine parameters, fuel economy and even the exact information of the cargo being transported.

Generally, aftermarket telematics solutions are implemented by local system integrators or dealers. Hence every time a customer brings up a different use case, SIs are ready to tweak their software by adding different features like new dashboards and reports. In many cases, hardware customisations are also implemented by integrating different type of sensors to the main unit; fuel, temperature, humidity, light, contact, pressure, weight, and tyre, to name a few

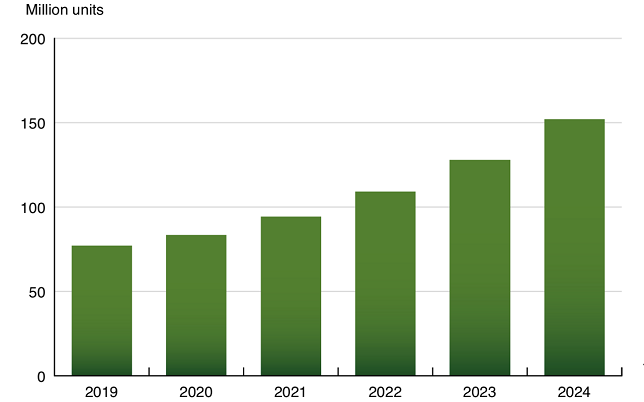

The addressable market for aftermarket telematics solutions is significant. At the end of 2019 just before pandemic, there were an estimated 1.12 billion passenger cars and light trucks registered worldwide. Even though aftermarket car telematics services face competition from smartphone- only solutions and OEM solutions, it is noted that the aftermarket telematics market is in a phase of strong growth. In a recent study report published by Berg Insights, it is estimated that total shipments of aftermarket telematics systems reached almost 24.7 million units worldwide in 2019. Growing at a compound annual growth rate of 14.4 percent, the shipments are expected to reach 48.5 million units in 2024. The number of aftermarket car telematics systems in active use is forecasted to grow at a compound annual growth rate of 14.6 percent from 77.1 million in 2019 to 152.1 million worldwide in 2024. The penetration rate will at the same time grow from 6.4 percent in 2019 to 11.1 percent at the end of the forecast period.

Stolen vehicle recovery and security-related telematics applications are mature aftermarket car telematics applications whereas other direct-to-consumer car telematics solutions have more recently started to emerge. Regional market conditions such as a high level of vehicle crime influence the demand for stolen vehicle tracking and have made SVT solutions popular in countries such as Brazil, Argentina, China, Israel, Russia and South Africa. The number of dedicated active aftermarket SVT units in use is forecasted to reach 68.6 million in 2024, up from 47.1 million at year-end 2019.

Challenges and Competition

As the market and demand grows for Telematics, its not just contributing to Aftermarket segments, OEMs and Smart Phone options are also equally emerging in the same way. However, the Aftermarket options make its value proposition distinct to others and hence it has build a different segment with its unique advantages

OEM Fitted and Aftermarket

Since the dawn of m2m revolution, it has become a priority for the OEMs also to have their part in Telematics, Volvos and Daimlers were the pioneers to add it to their vehicles. Volvo Dynafleet is an extensive and comprehensive solution, which captures even the minutest data from their vehicles and brings intelligent analytics out of it.

But now even simple scooters have become connected! They give their best information to the owners through a concise mobile application.

However, in a bigger picture this will not suffice the actual Telematics requirements of a Fleet Manager or an Organisation who really wants to use it efficiently. Prime reasons being

- Almost all major fleet companies and organisations operate multi-brand fleet. Hence its not possible to get everything under one umbrella. In simple words, Volvos doesn’t want to share their info to Daimler platform or even to a third party fleet management software. So, if a company with 5 different branded vehicles have to use 5 software platforms, which becomes really difficult to get meaningful reports and analysis out of it.

- After sales service and support is also a big challenge for OEM Telematics. For each and every support cases, customers need to bring the vehicle to dealerships and in many cases a dealer doesn’t have a proper service support team to solve customers queries about telematics software. On the other hand, aftermarket guys would be at your door steps for any service support and many cases they are ready to travel to remote locations where vehicles are currently placed.

- Customisation and Integration is also one of the biggest limitations of OEM options. Mostly all large fleet companies would have their way of operations and priorities. For example, some of them would need driver identification some other need passenger security options or in some cases it would cargo monitoring options like temperature, pressure, weight etc. Here no OEMs are going to customise their solution for such requirements. Hence aftermarket telematics is the only space where you can get your requirements clearly addressed.

Smart Phone Replacing Device Telematics

Since the Uber revolution began, Taxi aggregation concepts have changed the entire perspective of transportation, now days this concept have placed its strong foot prints in commercial transportation also. Here the entire show is apparently run by Smart Phones, and hence it is being said, this can be a big threat for Aftermarket Telematics Industry. But on the contrary, when we analyse the exact value proposition offered by two options, we can see a clear distinction in the very basic use cases itself.

- One of the main reasons for installing an external Location Tracking or fuel sensing device is to minimize the dependency in Drivers and hence make the entire fleet management operations automated. So to get this data from the very drivers phone doesn’t make any sense here!

- Majority of fleet managers prefer to install telematics solution not just to track the location of vehicles. They have much higher priorities like to get the engine status, idling conditions, Trip information, fuel levels etc. Such details cannot be pulled through a smart phone because this information depends on different inputs from the vehicle, which is not accessible by a phone.

- Confidentiality and Durability is another main reason for making device telematics distinct. Majority of the fleet companies wants the device to be inaccessible by the driver and has to be full time powered, so in most cases the devices are planted inside the vehicle body where it is kept well hidden and directly connected to the vehicle battery. Phones need to be recharged!

Hence such priorities will completely rule out the possibility of replacing device telematics with Phones!

The Real Revolution is only beginning

Although Aftermarket Telematics have been here for over 2 decades, its penetration and numbers compared to the total market size, is still very lean. Just consider the Indian market, still over 90% vehicles belongs to unorganised segment where things are happening very conventionally. Although we saw a slight change in this owing to the smartphone revolution, major crowd including individual vehicle owners still find it unappealing to adapt to the telematics age.

However, things took a drastic turn when governments started to make it mandatory to install Vehicle Location Trackers(VLT) in all vehicles, this brought a very big revolution in the market. Now that VLTs installation and service are seen as a basic need, it is becoming available even in very basic auto-electric shops. Since such rules have become new standards, people started to think what all options can we get on top of this, thus it is paving the for further integration like fuel, temperature, OBD etc. and there by exponentially growing different segments of telematics.

Outside of India, even countries like UAE, Saudi Arabia, Sri Lanka etc. are working on such legislations and even large corporations both public and private is following this way. So, by 2025 atleast 10 countries would be in its way to implement such rules followed by others shortly.

Although such implementations are done mostly for the security purpose, Telematics Solution providers and System Integrators are trying to add too many icings on the cake in-terms of features and value additions there by securing higher subscriptions with VAS. Many vehicle owners also feel they could get much higher value proposition by just spending 20-30% extra over the mandatory devices.

2G Sunset

As we all know, 2G spectrums are getting outdated and telecos have really started to think of their ROIs in maintaining this spectrum since usage of 2G mobile phones have slowed down drastically. So for them its better to convert them to 4G and 5G for better ROIs. In many countries 2G have become a memory literally! In some other they have declared the shutdown timeline and have asked customers to adapt to 4G or NBIoT.

This instigated another big revolution since all existing IoT installations have happened in 2G. Telematics being holding a major share in such installations gives a new opportunity for companies to replace such devices with 4G or other newer spectrum devices and hence add many great features like camera, hotspots, better battery life etc.

Recently a country happened to declare 2G-spectrum shutdown in 2023. Around 250,000 vehicles running in a single project have been ordered to change all its 2G devices with CATM1 standard models. This shows the kind opportunity being opening up across the world in next few years.

To summarise, its going to be a real revolution in next few years! As per a recent report, the number or vehicles with aftermarket telematics is going to become 150 million by 2024. Though post corona supply chain hassles for semiconductors have brought some headaches to the Telematics manufacturers, a new normal in post pandemic is quite promising for the Aftermarket Players.

References: M2M Research Series Report on After Market Car Telematics, Berg Insight.

Author:

Feroz Rehman

CEO

Transight Systems Pvt. Ltd

He Co-founded Transight Systems with Mr. Gis George, which has turned to be a Multi Multimillion Dollar Telematics Device Development and Manufacturing company from South India. He is keener on the Research and Development of new products, International Markets and formulation of business strategies in the company.

Published in Telematics Wire