Usage-based Insurance refers to the Connected Car (Telematics) technology used by Auto Insurers to provide accurate prices or new services to their customers. With evolving regulations and demand, Insurers are also introducing UBI in several emerging markets in the world.

Smartphone-based Telematics as the technology option for Usage-Based Insurance is a growing trend. Conventional UBI programs have relied on wired GPS or OBD dongle-based solutions to gather data from vehicles. They are still in use due to their reliability in capturing data from the insured vehicle without the driver’s intervention. But these come at the cost of adoption and logistical friction that has prevented mass adoption. App-based Telematics measures driving behavior using the driver’s smartphone sensor and GPS data. With no device, the solution becomes scalable, affordable and frictionless.

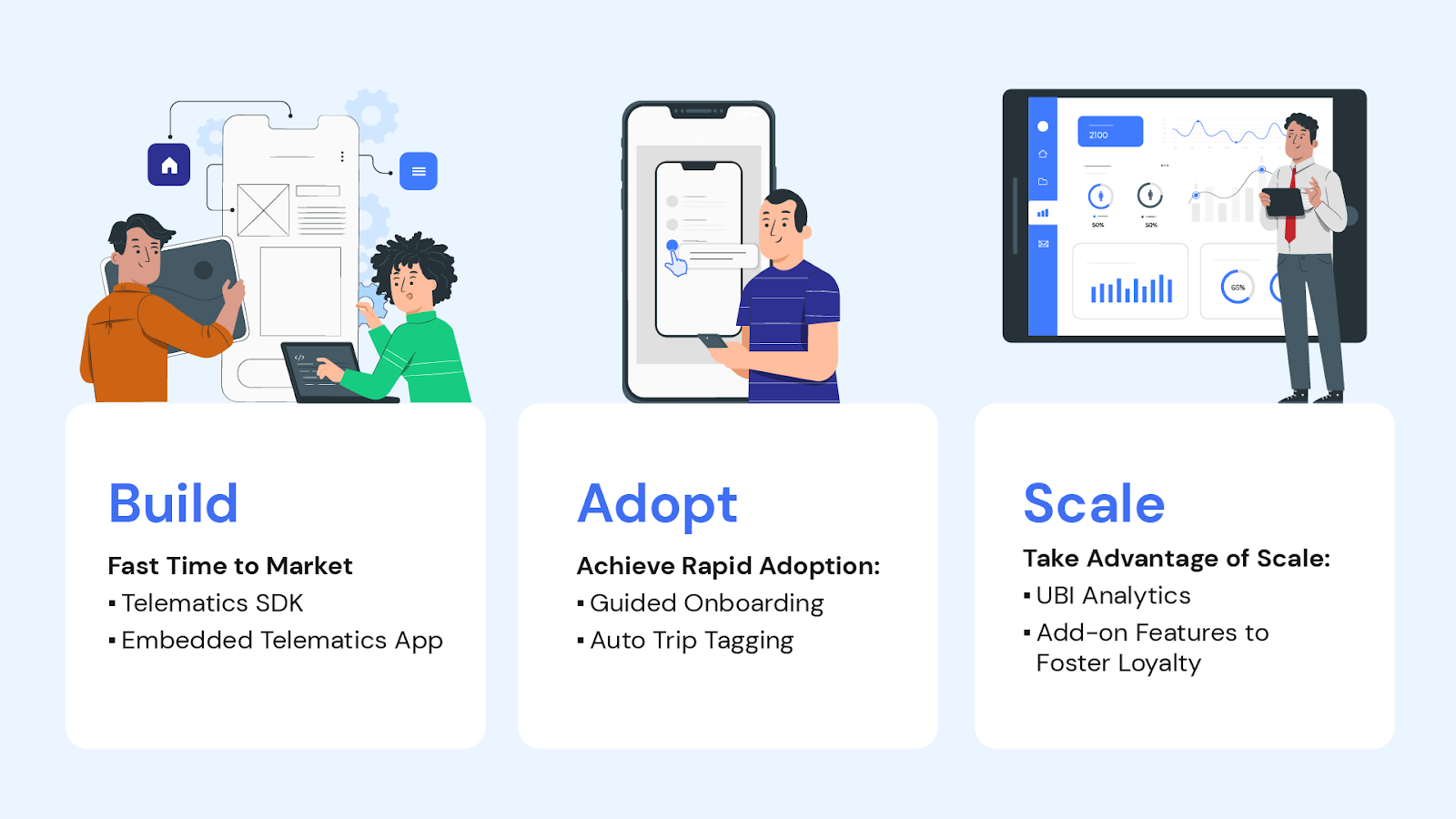

UBI is a strategic initiative for Insurers in a competitive environment, and hence the speed with which an Insurer can launch, get adoption, and scale their UBI program is key. This article offers some Technology best practices for Insurers to scale their Usage Based Insurance initiative via Smartphone Telematics across the phases of Build, Adopt and Scale.

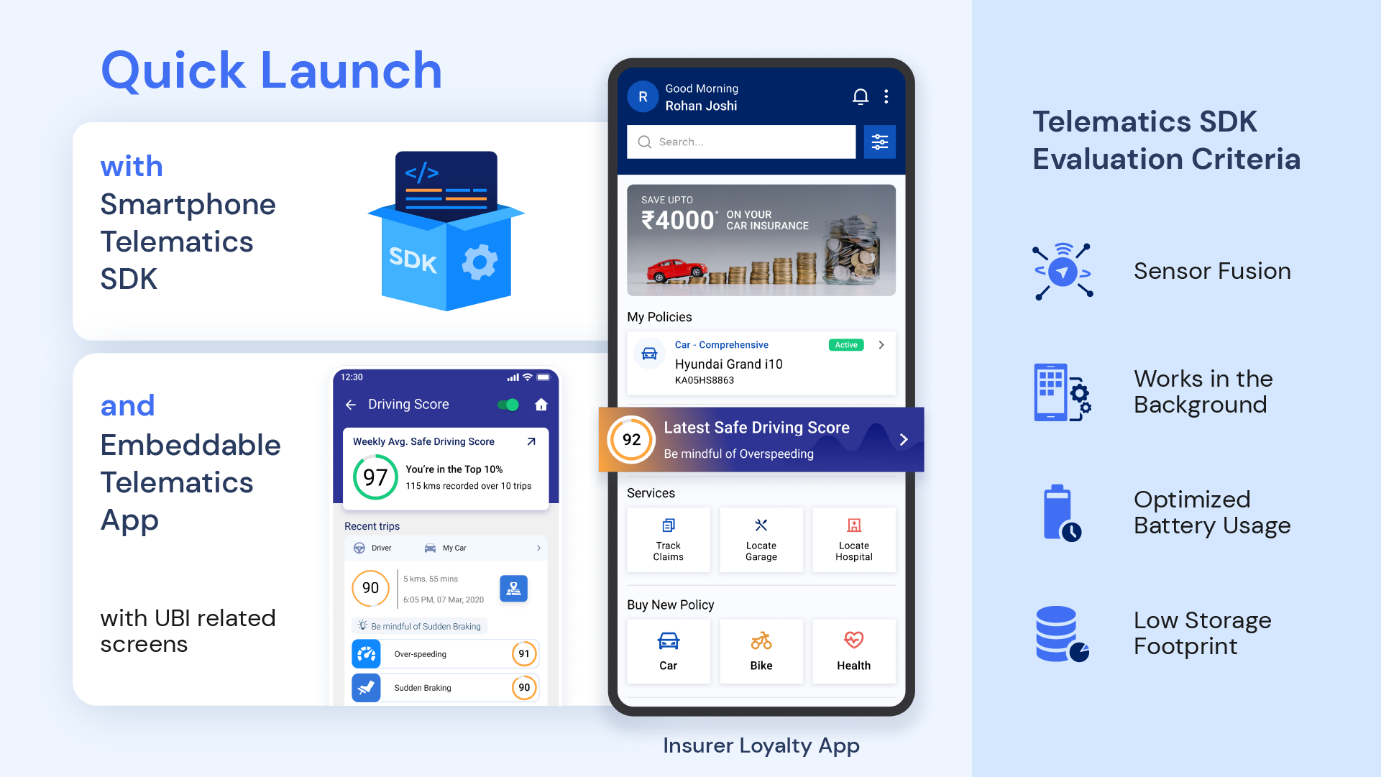

Build and Launch Fast with Telematics SDK:

Most Digitally forward Insurers offer a Loyalty App that offers ability for Customers to buy, renew Insurance as well as initiate and track Claims. Once an Insurer decides to offer a Smartphone based UBI Product, the best approach is to incorporate a Telematics SDK into the existing Loyalty App rather than develop a separate UBI App.

Telematics SDK from a Smartphone Telematics solution provider typically incorporates core smartphone sensor data capturing, processing and analytics inside a library that can be easily incorporated inside the Insurer’s App.

SDK should also handle the crucial usability aspects related to Smartphone telematics including:

- Sensor fusion and axis correction techniques to make best use of accelerometer and gyroscope sensors besides GPS data for accurate driving behavior detection

- Ability to auto-detect trip start/stop when User is driving and multi-trigger approach to gather data in background without App being open

- Optimized use of Smartphone Battery while still ensuring accuracy of data capture and driving behavior analysis

- Low storage footprint to not bloat the size of the Host App

- Support integration with multiple Platforms including native Android, iOS and other multi-platform frameworks like Flutter

SDKs still require Insurer’s technical team to integrate the APIs and develop customized User Interface which may take from anywhere from few weeks to few months depending upon the technical team’s readiness.

An even faster methodology to quickly launch a UBI initiative is to use Embeddable Telematics App inside the Loyalty App. Embeddable Telematics App is an SDK along with the required User Interface screens pre-built for the common UBI product scenarios such as Pay-As-You-Drive or Pay-How-You-Drive. With quick customizations, Embeddable Telematics App provide a truly low-code way for an Insurer to launch best-in-class Smartphone telematics within a few weeks.

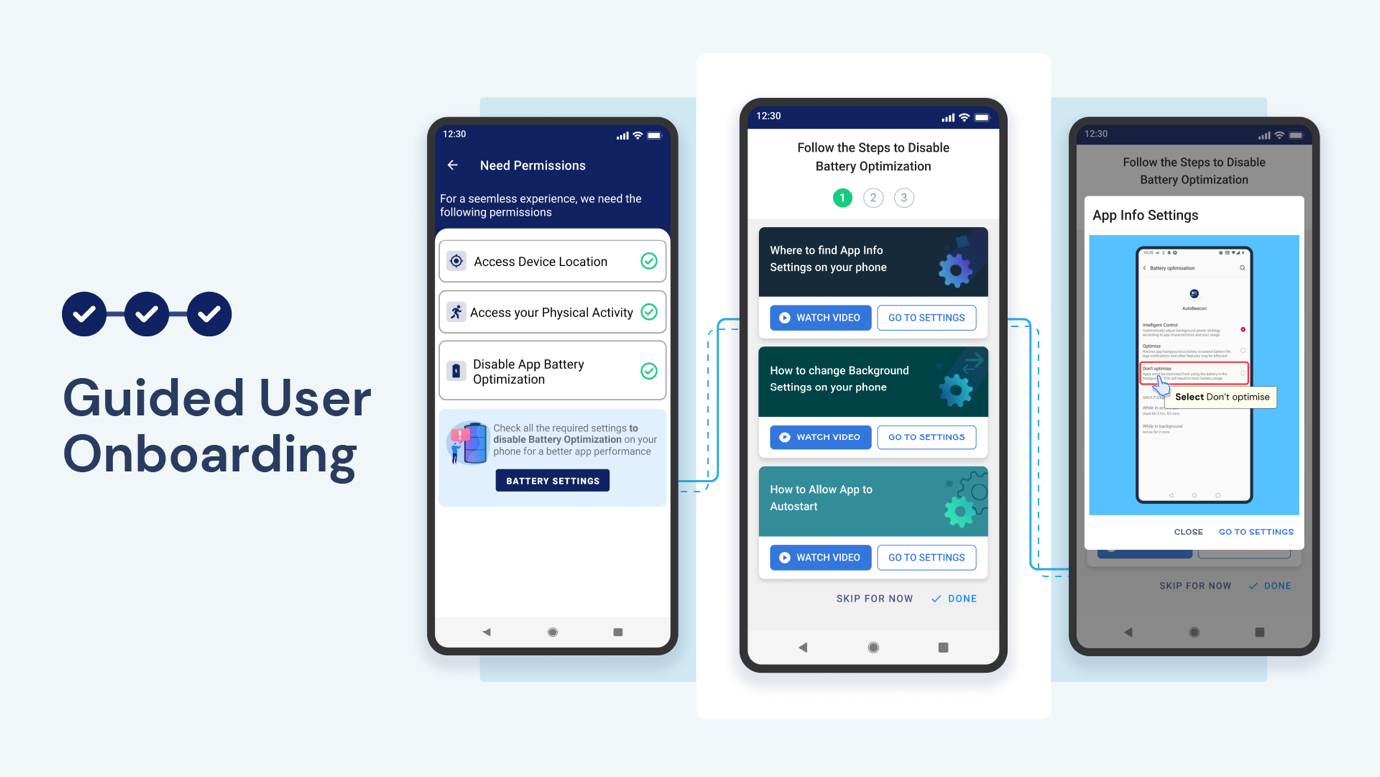

Overcoming Challenges related to Onboarding and Data Accuracy

Insurers need to be mindful of a few specific technical challenges they will encounter in field while using Smartphone Telematics for UBI

Self-service Onboarding

For Smartphone based telematics, it is expected that the App will work in the background and detect the trips automatically without user intervention. Modern Smartphone OS are designed to optimize Smartphone battery and don’t allow App to collect GPS and other sensor data in the background.

Hence, User needs to grant certain specific permissions to the App in order for the UBI App to work seamlessly. These permissions vary from Smartphone Make and OS version. In emerging markets with fragmented market share of Android Smartphone Makes with their own variants of Android, this issue is even pronounced.

To address this challenge, Embeddable Telematics App needs to have an onboarding process that automatically detects specific Smartphone Make and OS version and provides a guided flow to the User for granting the various permissions. Server side mechanisms can track the permission status dynamically for each onboarded user and notify user if some setting is missing. These mechanisms ensure that Users are successfully self-serviced and reduce the burden of customer support in successfully onboarding the Users.

Automatic Tagging of Trips in Insured Vehicle

Since Smartphone Telematics App shall record journeys of Users in any automotive vehicle, App needs mechanism to identify trips which have been taken by the Insured in her own vehicle, as those are the ones which are of interest to the Insurer from UBI perspective.

Best practices around solving this technical challenge include the following:

- For vehicles with Head-unit or Infotainment Unit with Bluetooth interface, App can automatically identify journeys in User’s own vehicle

- Alternatively, a small, low power BLE Beacon can be placed in the vehicle to achieve this Auto tagging and ensure that only valid driving data from that vehicle is scored.

- Yet another alternative is to use Artificial Intelligence techniques to classify the trips taken in own vehicle vis-à-vis other modes of transport such as taxi, bus and train etc. These AI models learn the pattern of driving behaviour of the Driver in her own vehicle over an initial number of journeys and then use that model to auto classify the subsequent journeys.

At-scale Analytics and Engagement Features to drive Retention

After an Insurer has quickly launched and smartly gained adoption of customers using the best practices discussed above, Smartphone Telematics presents the real opportunity for the Insurer to really blitz scale the initiative.

At scale, Smartphone telematics generates a treasure trove of data that Insurer can leverage for building under-writing models that better predict risk. At this stage, Insurers Underwriting and Actuarial teams need scalable business intelligence dashboards that offer aggregated insights derived from granular data of entire customer base. Ideally, such UBI dashboards should provide fast and updated Analytics sandbox that Insurer’s analysts can use to slice-and-dice driving behavior trends across a variety of dimensions including demographics, location, driving risk variable and so on. Correlation of such risk scores with Claims data will enable Insurers to fine tune premium pricing that matches the true risk and build a long-term competitive advantage.

At the same time, a scalable Customer/App Analytics engine can enable product teams to understand App usage patterns of different customer segments and offer add-on In-App features that encourage Users to engage with the App. These include customized tips for Eco-driving based on Driving Behavior, personalized Driving behavior alerts and Leaderboards/micro-rewards to gamify the Driving Behavior Score. Insurers can offer Value Added services based on Smartphone Telematics such as Automatic Crash Detection and emergency support. All these features along with the core UBI offering drive customer retention and loyalty.

With Smartphone Telematics embedded inside Insurer’s Loyalty App and carefully nurtured using the best practices described above, Insurance is not something the customer buys and forgets but becomes a constant companion.

By deploying the above best practices, early moving Insurers can successfully launch and scale UBI initiative in emerging markets and achieve sustainable lead over competition.

Author:

Kamal Aggarwal

Co-founder and CEO

SenSight Technologies Private Limited

Kamal Aggarwal is Co-founder and CEO of SenSight Technologies, a start-up working at the intersection of Automotive IoT and Big Data. SenSight’s AutoWiz Connected Vehicle Data Analytics Platform powers use cases for players in the Automotive, Insurance and Shared Mobility domain. SenSight’s AutoBeacon Smartphone Telematics solution enables Insurers to offer Usage-Based-Insurance products and increase customer engagement. Kamal has 20+ years of experience in Strategy, Marketing and Product Management for high tech ventures.

Published in Telematics Wire