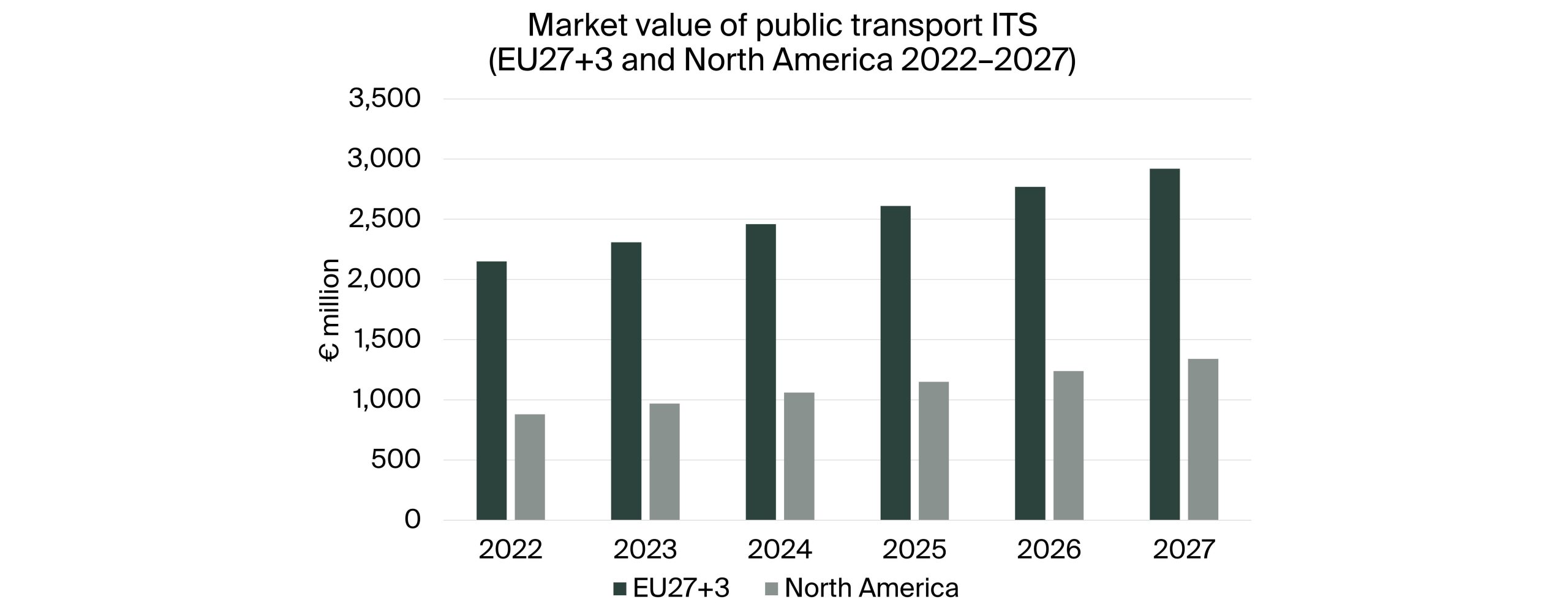

Gothenburg, Sweden – March 15, 2024: Berg Insight, has released new findings about the market for Intelligent Transport Systems (ITS). The estimated market value for ITS deployed in public transport operations in Europe was € 2.15 billion in 2022. Growing at a compound annual growth rate (CAGR) of 6.3 percent, this number is expected to reach € 2.92 billion by 2027. The North American market for public transport ITS is similarly forecasted to grow at a CAGR of 8.8 percent from € 0.88 billion in 2022 to reach € 1.34 billion in 2027.

Berg Insight is of the opinion that the market for ITS in public transport is in a growth phase which will continue throughout the forecast period. Considerable investment is going toward electrification of the public transport fleet, which will require more sophisticated ITS solutions to operate smoothly. In addition, the increasing demands from travellers for convenience and accessible real-time information contribute to a positive market situation. Governments in both Europe and North America view public transport as a prioritised area for investment. The Canadian government has for example announced a CAD 2.75 billion (€ 2.0 billion) investment toward electric buses, school buses and related charging infrastructure between 2021–2026.

A group of international aftermarket solution providers has emerged as leaders on the market for public transport ITS. Major providers across Europe and North America include Canada-based Trapeze Group. Germany-based INIT also has a significant installed base in both regions. Clever Devices and Conduent hold leading positions on the North American public transport ITS market. The former has expanded into Europe with an acquisition and the latter is an international provider of fare collection systems. Additional companies with notable market shares in North America include Cubic Transportation Systems and Avail Technologies.

Siemens Mobility is a prominent vendor of software in both Europe and North America. Examples of major vendors on national markets in Europe include EQUANS and RATP Smart Systems, which hold leading positions in France. IVU is an important player primarily in the German-speaking part of Europe. Vix Technology, Flowbird and Ticketer are moreover major providers on the UK market. Other significant players include the Spanish groups GMV, Indra and Grupo ETRA; French Thales; Atron in Germany; Scandinavian FARA, Pilotfish and Consat Telematics; and Austria-based Swarco and Kontron Transportation. Volvo Group and Daimler are moreover notable players from the vehicle OEM segment. Companies such as Scania, Iveco, Gillig, and New Flyer also offer some conventional OEM telematics features for their buses.

“We increasingly observe that developers are creating solutions with standardization and interoperability in mind. ITS solution providers are now for example commonly requesting labels of compliance from standard organisations” said Caspar Jansson, IoT Analyst at Berg Insight. Interoperability opens up many new possibilities for various stakeholders in the ITS ecosystem. “The standardisation efforts enable public transport agencies to combine competitive solutions from multiple vendors in their networks. The issuing authorities have now issued the first tenders explicitly requiring equipment to comply with the ITxPT standard”, concluded Mr. Jansson.