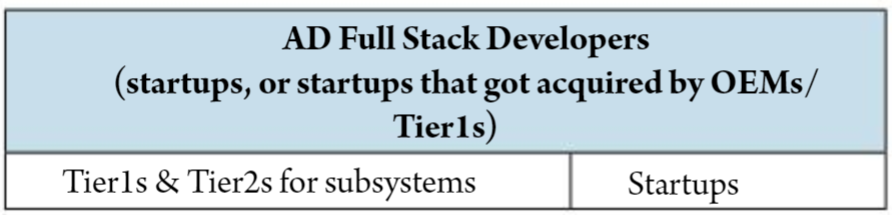

For the past 5 years, venture capital investment in AD/ADAS ecosystem was heavily skewed towards Automated Driving (SAE levels L4/5). This was driven by the belief that large-scale deployment of AD deployment was imminent.

Several startups emerged and raised capital in the order of billions of dollars, i.e., Cruise, Zoox, Auro, Aurora, Nuro, TuSimple, to name a few. These companies focused on the full stack for various vehicle segments.

Along with these full stack companies, other startups have focused on specific elements in the AD Tech Stack such as 3D Navigation, Lidar and 3D Radar.

The AD technology development ecosystem

Shifting timelines and capital-intensive nature of AD industry made this approach an unsustainable game. As positive cash flow forecasts continue to push out few Full Stack players, only those who raised ton of capital, are able to survive.

As the hype for AD tempered a little, startups and VCs instead have shifted the focus towards ADAS (SAE L1 to L3), in search of next big growth opportunity. In part this is because of the greater degree of specific value that a start-up can develop with an acceptable level of investment and within a more reasonable timeframe. The rapid near-term growth of ADAS makes it an attractive opportunity for startups.

ADAS is estimated to grow at double digit CAGR reaching to a market size of > $90 Billion by 2030 (source: UBS). The strong growth is driven by consumer pull for ADAS functions such as Automated Parking, Lane Assist, Adaptive Cruise Control, Collision Warning and Mitigation, Driver-Alert, Front and Rear Object Detection, Pedestrian Detection, Blind Spot Warning, Reverse Parking etc. up to Highway Chauffeuring.

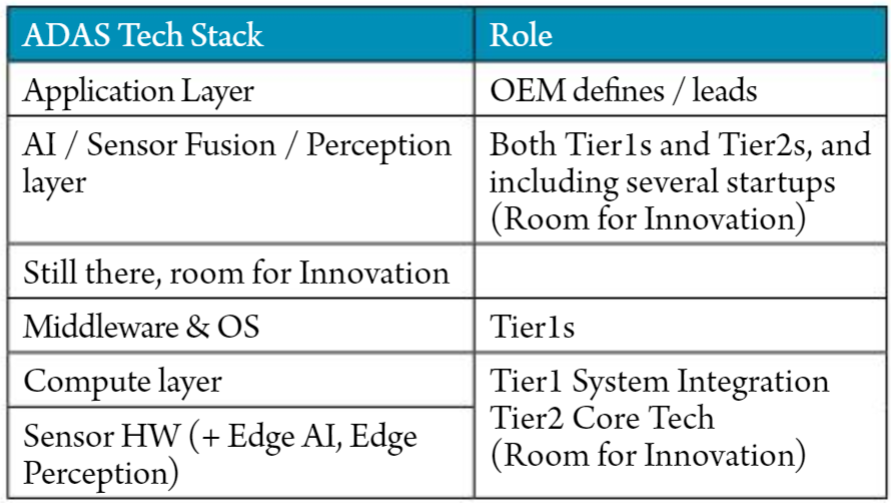

Opportunity in ADAS stack

To identify high value opportunities, startups must understand both the Tech Stack and the business value chain of ADAS system.

ADAS stack comprises of several layers from Application layer down to Hardware layer. OEMs are more active in the higher layers of the stack and the lower layers are served by Tier1s and Tier2s.

Startups have opportunities across the stack, and in particular AI/Sensor Fusion/Perception layer, Compute Layer and associated Tool Chains.

Opportunity in Tool Chains

In addition to the tech stack, there are new tool chains required to handle the massive data generated by the ADAS sensors and enable the AI training for developing the Perception layer, either on-prem or public-cloud.

While Simulation has been a focus area, Cloud companies are aggressively pushing into the AD/ADAS Tool Chain. While cloud providers have expertise in data management and tool for AI/ML development, they lack the subject matter/domain expertise that is essential to identify and solve niche high value

problems within the AD/ADAS data stack. This is another area where AD/ADAS startups can potentially excel.

Tool Chains

| @ On-Prem / Edge |

| Data Management |

| ML Ops |

| Simulation |

Author:

Anil Rachakonda is a Vice President at co-pace, a corporate program of Continental AG, focused on creating new product portfolio and onboarding disruptive innovation through partnership with startups. At co-pace, Anil heads Strategy and Analysis world-wide.

Prior to Continental, Anil was at Google where he led Partnerships at Advanced Technology and Projects group focused on the Smartphone ecosystem. Previously Anil was at Global Foundries (a portfolio of Mubadala), Applied Materials and Analog Devices in Corporate Strategy, Product Management and IC Design roles respectively.

Published in Telematics Wire