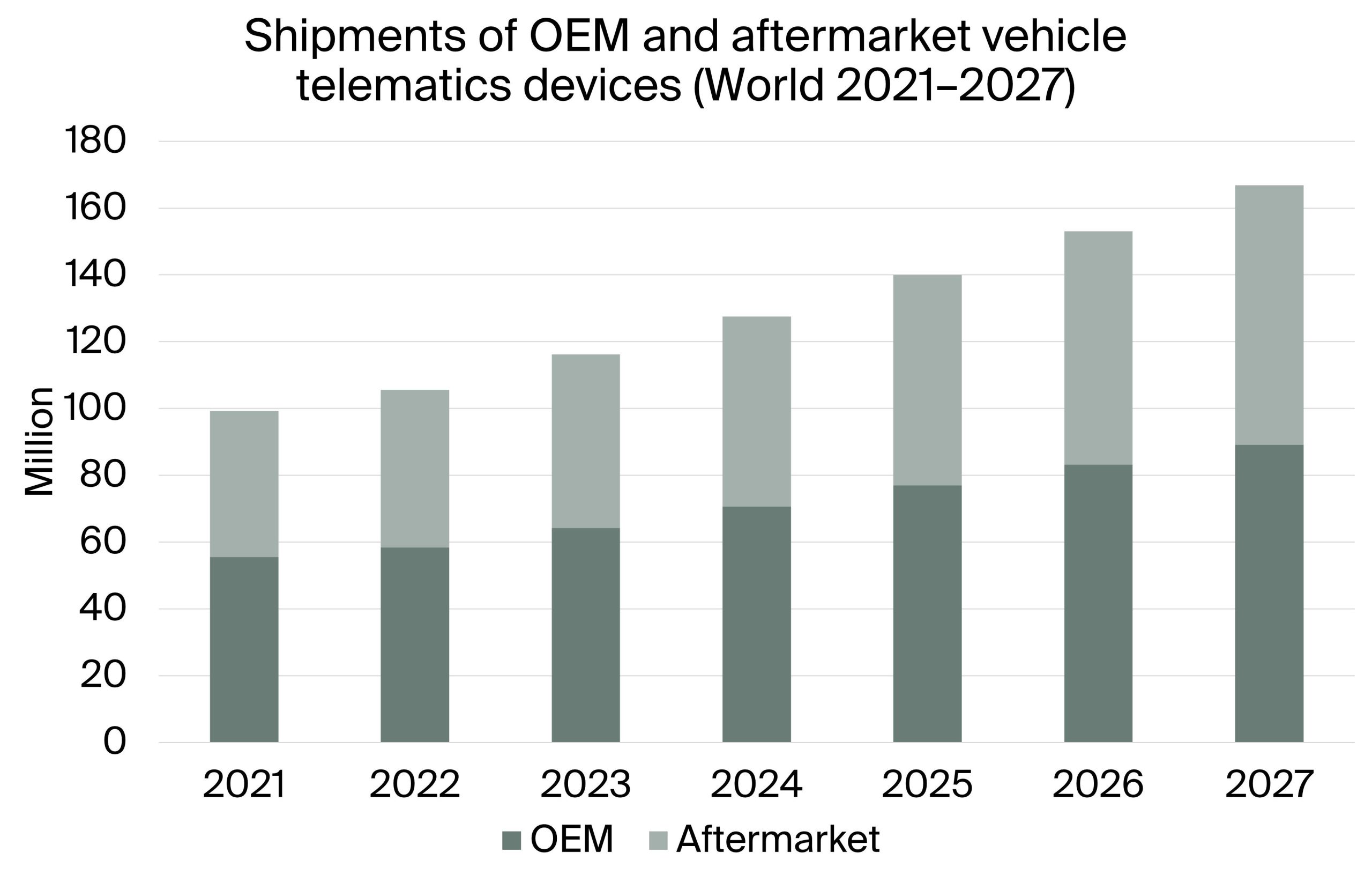

Gothenburg, Sweden – November 1, 2023: Berg Insight released new findings about the vehicle telematics hardware market. The global sales of aftermarket telematics devices surpassed 47.2 million in 2022, generating a market value of € 2.4 billion. The performance of the market was still affected by the COVID-19 pandemic and the following supply chain crisis. However, the market has shown recovering signs in 2023. The forecast indicates that annual shipments of aftermarket telematics devices will grow at a compound annual growth rate (CAGR) of 10.5 percent until 2027. At the end of the forecast period, we expect the shipments to reach 77.6 million. Berg Insight estimates that global shipments of OEM telematics hardware for passenger cars, light trucks, and commercial vehicles reached close to 58.4 million units in 2022. This corresponds to a market value of € 8.4 billion.

A combination of commercial and regulatory drivers now encourages a broader set of carmakers to expand availability of connected car services across geographies. This expansion is seen in various market segments. There are also numerous OEM telematics offerings from commercial vehicle manufacturers. Forecasters anticipate that the attach rate for embedded telematics devices among passenger cars, light trucks, and commercial vehicles will rise from approximately 72 percent in 2022. The projection indicates that it will reach 93 percent in 2027.

“Berg Insight ranks Teltonika as the market leader in the aftermarket telematics hardware segment. Teltonika reached telematics hardware sales of € 139 million”, said Martin Cederqvist, IoT Analyst at Berg Insight. Other vendors that hold significant market shares are CalAmp, Queclink, Jimi (Concox) and ERM Advanced Telematics. These five vendors generated together approximately € 483 million in annual revenues from the sales of aftermarket telematics devices. CalAmp has transformed from a pure hardware provider to an end-to-end solution telematics provider. The company is, however, still a major supplier of hardware telematics. It shipped 1.5 million units during 2022, corresponding to sales of €105 million. “Other significant aftermarket telematics hardware vendors include Sensata Insights, Positioning Universal and Danlaw from North America; Suntech International, Gosuncn RichLink, Neoway Technology, Gosafe, Kingwo, ATrack and iTriangle from Asia-Pacific. European vendors in the field are Meta System, Ruptela, and Munic.”, continued Mr. Cederqvist.

The design and development of OEM telematics systems is complex. These systems have to integrate with vehicle systems, fulfill strict quality standards, and ensure performance during the long lifecycle of a vehicle model. Generally established automotive suppliers that develop their solutions in cooperation with car manufacturers are the suppliers of OEM telematics equipment. “Shipments of OEM telematics hardware for passenger cars and light trucks amounted to about 50.3 million in 2022. This represents more than 86 percent of the total OEM telematics hardware shipments.”, said Mr. Cederqvist. The leading OEM telematics hardware vendors in terms of unit shipments are found in the passenger car segment. They are also prominent in the light truck segment. Examples of leading automotive suppliers of OEM telematics hardware include LG Electronics, Continental, Harman Marelli, Denso, Valeo, Actia, Lear, Bosch, Hyundai Mobis. Visteon and Aptiv are also notable suppliers in this category.

Download report brochure: The Global Vehicle Telematics Hardware Market