Pay-As-You-Drive, Pay-How-You-Drive are some of the innovative Insurance products that allow Driver or Vehicle owners the option of having premiums tailored to their individual driving patterns. Such products have been pioneered in the US market since mid-1990 when Progressive Insurance introduced usage-based products. Insurance Regulatory and Development Authority of India (IRDAI), in June 2022, has given the green signal for similar innovative products to be introduced by Insurance companies in India. All these innovative Insurance products require advanced technology solutions to provide necessary insights into usage patterns as well as to alleviate concerns like fraudulent claims.

Technology adoption in Global Insurance markets

Traditionally, telematics devices have been deployed in global markets to aid Insurance use cases. Telematics based insurance policy adoption rates are steadily increasing in the global insurance markets. Introduction of telematics in insurance has enabled insurers worldwide to price policies according to usage and driving behavior. Summarized below is the telematics insurance landscape in the USA, UK, and EU:

| Footprint in the US & UK markets | USA | EU and UK |

| In force Telematics policies: Q4 FY 2019 | 14.7M | UK: 1M, EU: 12.8M |

| Forecasted Telematics policies: FY 2024 | 53.6M | 44.5M |

| Projected Growth: CAGR | 29.6% | 28.2% |

Telematics has also resulted in numerous benefits for insurers including improvements in Loss Ratios, reduction in claim counts and average claim size, reduction in claim processing time and reduced rates of fraudulent claims.

The graph below shows the reduction in Loss Ratio for two leading USA insurers (State Farm and Geico) after telematics implementation

Can technology do more?

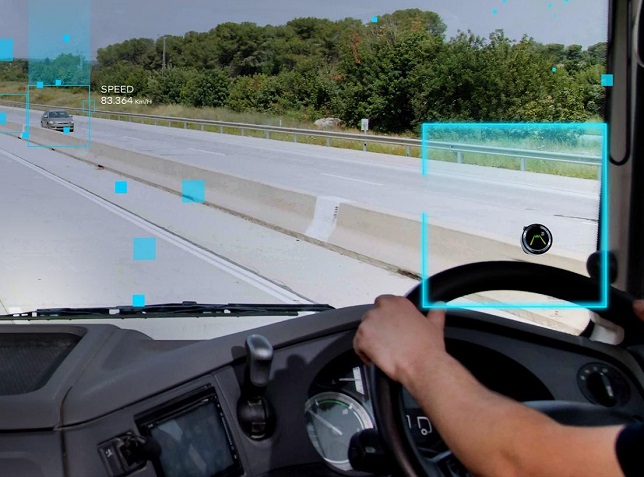

Telematics devices provide detailed insights into vehicle usage like number of kilometers driven, breaking and acceleration patterns, granular insights on vehicle condition etc. Such devices thus help derive a pattern of vehicle usage and are useful to define vehicle-based Insurance policies or Pay-as-you-drive policies. However, what is still missing are insights into driver behavior or performance. The better and safer you drive, the lower the risk for Insurance companies and allows further customization of motor insurance policies. Preventive safety technology such as Advanced Driver Assist Systems (ADAS) help understand driving behavior as it generates numerous safety related events which reflects how the vehicle is driven. One can argue, as a result, that Telematics devices are better suited for vehicle-based Insurance policies while insights from ADAS devices are better for Driver based Insurance policies. A solution that combines both is however the recommended solution as it provides the insurance company 360-degree view on both the Vehicle and the Driver.

Indian Motor Insurance context

India’s gross direct premium share in the global life insurance and non-life insurance market in the financial year 2019-20 was 2.73% and 0.79% respectively. Share of non-life direct premiums is 25.06% of which motor insurance was 32.59%. Annual growth rate for motor sector in financial year 2010-20 was 16.2% and is projected to be 6-8% for FY 2022-23. The top five insurers by gross direct premium written are ICICI Lombard, Bajaj Allianz, Tata AIG, IFFCO Tokio, and HDFC Ergo. The key players in the digital insurance and Insurtech space are Acko Insurance, Digit Insurance, and Navi Insurance 3,4.

The key challenges currently faced by insurers include:

- High Loss Ratios: The Indian Motor Insurance market’s historical Loss Ratios are higher compared to developed markets like the US and UK

- One of the key reasons identified for such high Loss Ratios was low-quality data leading to pricing model limitations

- Suboptimal Policyholder Utility Product innovation has been limited leading to policyholder dissatisfaction

- Lack of proactive connectivity with policyholders to ensure their safety and comfort while utilizing the insurance policy

The table below shows the average personal auto Loss Ratios for USA, UK, and India for Financial Years 2018-20 2,3,4:

| Loss Ratio | FY 2018 | FY2019 | FY2020 |

| USA | 60.15% | 60.62% | 53.52% |

| UK | 67% | 68.17% | 58.27% |

| India | 79.27% | 76.43% | 77.13% |

3 IRDAI annual report 2019-20,

4 https://www.coverfox.com/articles/the-growth-of-motor-insurance-in-india

India gears up for Road Safety Technology in vehicles

In Indian Motor Insurance context, technology adoption is still at a nascent state. Telematics solutions have been deployed in multiple pilots and data has been analyzed to understand vehicle usage patterns.

Trials have also been conducted to understand impact of preventive safety technology such as Advanced Driver Assist Systems (ADAS) on Insurance pricing. Early pilots have shown up to a 15% reduction in Insurance claims post ADAS adoption.

At Intel, our vision is to help prevent road accidents before they claim lives and livelihoods. Advancing the use of technology for road safety, Intel® Onboard Fleet Services is a comprehensive fleet safety solution that brings world-class and road-tested technology exclusively to Indian commercial vehicle fleets. It offers Collision Avoidance Systems (CAS), Driver Monitoring Systems, Fleet Telematics, Vehicle health, and Fuel efficiency features. Powered by a portfolio of in-cabin devices, Intel® Onboard Fleet Services has a state-of-the-art cloud portal that includes actionable insights, analytics, and reports for fleet managers. At the heart of the solution is driver coaching, which activates 15 different inputs to provide individualized coaching recommendations to drivers.

Challenges to technology adoption

In Indian Motor Insurance context, technology adoption is still at nascent state. This is because adoption of novel technology cannot happen unless that technology is localized to specific deployment context and the local market dynamics.

Intel along with EOX Vantage conducted a 6-month study on business and technology challenges that need to be addressed to promote adoption of preventive safety technology such as Advanced Driver Assist Systems (ADAS) for Personal Vehicles by Insurance companies. The study also investigated how the resulting new-age insurance products can be structured in terms of gains to various stake holders involved – Insurance company, Vehicle Manufacturer, Vehicle Owner, and Technology provider. The study highlighted multiple challenges that need to be addressed for successful adoption of technology for business outcomes.

Key findings

- Benefits will be realized over longer term: The technology is expected to provide benefits over the life of the policy, for instance, 3 years to 5 years, whereas the cost of technology will be upfront. So, the time value of the benefits will be lower if device cost is paid for upfront. There is also a risk of policyholders leaving the insurance company within a year or two as they are sensitive to premiums. Hence customer retention measures are required in tandem, to realize expected long-term benefit from technology adoption.

- Thin profit margins limit the ability to accommodate additional technology costs: The Motor Insurance Personal Vehicle market in India is highly competitive and running on profit margins too thin to accommodate technology costs even if there is an expected reduction in Loss Ratios. Innovative financing schemes for technology products need a closer look here.

- Benefits may not accrue to the entire portfolio: The cost of technology will be justified for portfolio segments where the premium size could be higher relative to the cost of technology. For instance, the technology could prove to be adding value for the high IDV segments. Such segments are not a major part of the auto insurance portfolio for most of the insurance companies. Insurers seem to be looking for a solution that can be applied to a substantial part of the portfolio.

- Technology installation and/or maintenance issues: Insurance companies lack expertise in managing the logistics of technology, including installation and maintenance of the technology, so there may be concerns associated with the logistics aspects.

- Regulatory Issues: The implementation of the proposition could lead to policyholder grievances and IRDAI objections around the data privacy.

The way ahead

There is a need to create cost-effective and innovative technology adoption models. Pragmatic implementation models need to be carved out so there is an equitable distribution of return on investments among the various entities in the ecosystem. Some of the models could be:

- Offering vehicle safety technology via OEMs

- Offering DaaS (Device as a Service) to insurance companies for a fixed charge

- Providing underwriting support through Driver Risk Score, developed using the data recorded by safety technology

- Educating policyholders, insurers, and the regulator how the data will used

- Working with the insurers and the regulator to design pilots to testify the proposition before full-blown adoption

The current state of the Indian Motor Insurance market does indicate willingness of Indian insurers to take risks in committing to technological innovations like Vehicle telematics and preventive safety technology such as Advanced Driver Assist Systems (ADAS). Such technology adoption could lead to long-term financial benefits. However, the market is also characterized by very low profit margin which is severely limiting their ability to bear the cost implications of such innovations.

The ability to take such risks can, however, be made to increase if the proposition could be designed in a way that there is more equitable distribution of the associated costs and risks among all the parties involved.

Authors:

Raghavendra Bhat, Anbumani Subramanian & Juby Jose, Intel Corporation

Ankush Agarwal – Partner, Machine Learning at EOX Vantage

Published in Telematics Wire