The new digital age has already transformed many industries from entertainment to automobile and banking sector. The insurance industry is also adopting digitalization to improve business operations and offer innovative and better solutions that give more value to the customer. This ever-growing digitalization is anticipated to offer solutions that will improve consumer satisfaction in the coming years. The customer value has always been all-time low with high turnover in the market along with low trust and ultimately no loyalty to the insurance organizations. Using the new digital technologies, the companies are expected to offer greater value by building trust with the policyholders along with the engaging experiences that can lead the market towards uberization.

The key reason why traditional insurance system is unable to change the game is that it could not improve customer interactions over the past years, which is anticipated to get an overhaul with the smartphone-based solution called Telematics. Telematics solutions enhance the regularity and richness of customer interaction that leads to improved customer relationship. This is anticipated to improve customer satisfaction and loyalty which can provide impetus to the growth of the insurance companies operating in the market. As the customers migrate towards smarter solutions catering to their personal preferences and requirements, insurance organizations would have to leverage the opportunities provided by telematics.

Insurance telematics is widely utilized to track the driving pattern of the users by collecting, measuring, and transmitting several data points with a small GPS-based device mounted inside the vehicle. It also traces the driving pattern of users by analyzing the data points related to braking, cornering, speed, and location of the vehicle. Insurance telematics enables organizations to implement usage-based insurance (UBI) programs across their customer base by supervising the performance of the drivers behind the wheels. Equipped with more data and insight, UBI programs have the potential to overturn the traditional auto insurance business models.

The insights generated by smartphone based UBI solution system can be used to correlate directly to the underlying road network to provide financiers the ability to deduce the adaptation of the user to their environment. The live telemetry data can be meshed with the external sources of data to extricate information related to the drivers and their behavior.

The pricing method for UBI greatly differs from that of traditional auto insurance system which is simply calculated based on data including historical accident rates, driving records, vehicle type, zip code, age, gender, etc. Traditional auto insurance depends on actuarial studies of accumulated historical data to generate rating factors that incorporate driving record, credit-based insurance score, personal characteristics, vehicle type, garage location, vehicle use, previous claims, liability limits, and deductibles. Premium discounts on traditional auto insurance are usually restricted to the bundling of insurance on multiple vehicles or types of insurance, insurance with the same carrier, protection devices, driving courses, and home-to-work mileage.

The insurance telematics includes mainly two types of the products which are:

- Pay As You Drive (PAYD): PAYD is the usage-based product. It is the kind of comprehensive car insurance plan that charges a premium based on the usage of the car. It basically uses the telematics device to monitor the dependency of the time the car is used on the total number of kilometers covered.

- Pay How You Drive (PHYD): PHYD is the user behavior-based product that solely depends on the driving score of the user. It is the telematics-based car insurance plan for which the premium is calculated depending on the driving style of the car.

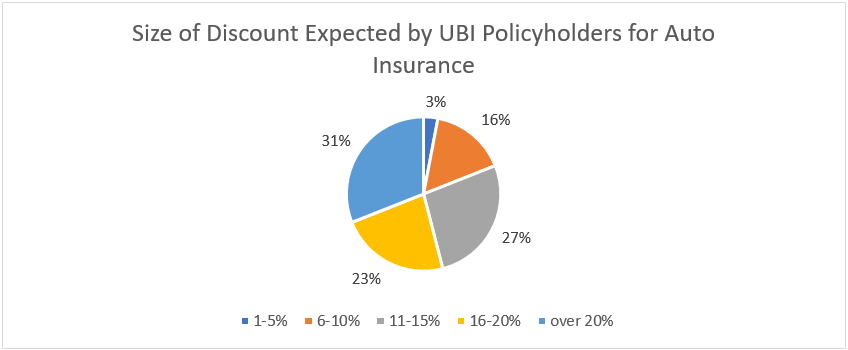

Transforming insurance into the variable cost, with the promise of some cost savings is expected to hold major appeal for policy buyers who treat motor insurance as an indisputable annual fixed cost. It is estimated that the UBI system can reduce accident rates by 10%-40% with substantial benefits for the individual and society. From the perspective of an insurance provider, telemetry data maintains the promise of altering premiums based on the risks that the business demonstrates.

The burgeoning insurance telematics demand is attributed to the escalating need for compliance and regulations, reduction in cost of connectivity solutions and the rising demand for risk assessment and management. The structure of automotive insurance such as collision, liability, and third-party insurance for both established and emerging economies is expected to generate the demand for telematics in the coming years. The humongous growth of insurance telematics is also supported by several factors including low premiums and vehicle tracking during theft along with the personalized and value-added services in insurance plans to cater to the customized needs of buyers. Moreover, the emergence of IoT and cloud computing has presented many opportunities for the innovations in insurance telematics across the globe.

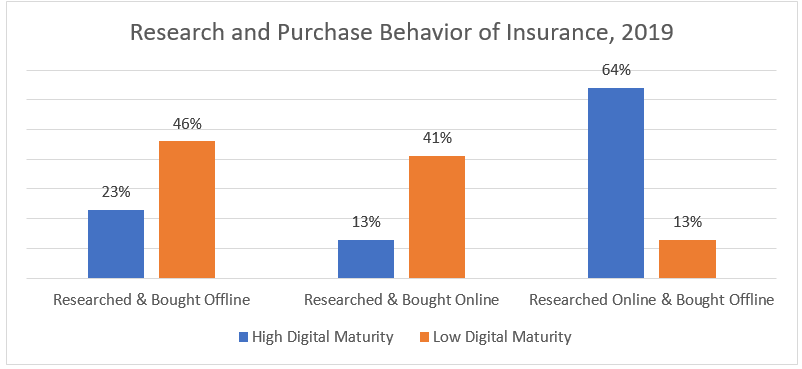

The Indian consumers are the second most active out of all countries in APAC when it comes to searching for and purchasing new insurance policies. Additionally, the COVID-19 pandemic has contributed to the accelerated use of digital platforms in India, offering insurance companies a medium to connect with the customers.

In India, the insurance telematics market is estimated to witness a steady growth in the next few years due to the rising concern for safety and security among people. The information from the insurance telematics system is useful in several circumstances which includes connecting with the police and hospital immediately in case of an accident for swift response. These factors are anticipated to drive the growth of the Indian insurance telematics market in the forthcoming years.

However, sharing location data of the vehicle using GPS and onboard diagnostics has emerged as a key concern among consumers, pushing them to rethink about sharing the personal data. Additionally, implementing a UBI program can be costly and resource-intensive to the insurer as the programs rely heavily on the expensive technology to capture and sensitize the driving data. However, new innovations and technological advancements are anticipated to eliminate these restraints over the period.

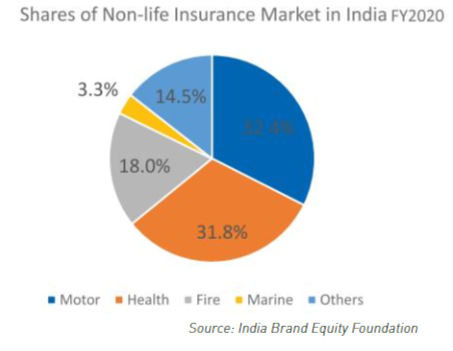

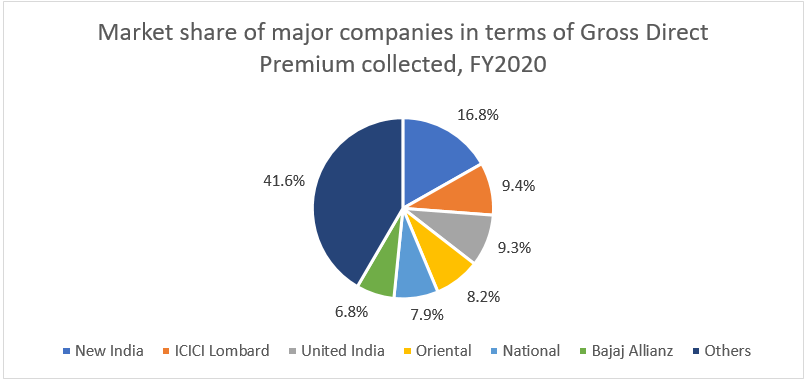

Bajaj Allianz General Insurance Co. Ltd, Bharti AXA General Insurance Co. Ltd., ICICI Lombard General Insurance Company Ltd., Tata AIG General Insurance Company Ltd, HDFC ERGO General Insurance Company Ltd., New India Assurance Co., Oriental Insurance Co. United India Insurance Co., Reliance General Insurance Company are some of the major players in the motor insurance industry in India. The companies are investing more to develop new technologies to increase their customer base and expand their geographic reach.

The Insurance Regulatory and Development Authority of India (IRDAI), on November 25, 2020, proposed a draft proposal that is in favor of the usage of the digital telematics-based car insurance system. With the top insurance bodies in the country encouraging insurers to use the insurance telematics, the major vehicle insurance companies are anticipated to enroll such policies in the future. Many insurers have initiated accepting insurance telematics policies, however, acceptance among stakeholders at different levels would take time.

Bajaj Allianz General Insurance Company introduced pay as you use car insurance in India for the first time in May 2020, offering car owners a flexibility to insure their vehicles for shorter time instead of the full year. Bajaj Allianz also launched a DriveSmart Service in 2016 which uses telematics to enhance customer safety and promises to lower the premiums. The key features of the service include geo-fencing and tracking, vehicle diagnostics, driving pattern and statistics and document wallet.

Despite of it being at a nascent stage, telematics-based car insurance is receiving a traction from many vehicle owners. Though car drivers are skeptical about its usage, it is expected that as we move forward, it will gain more acceptance among the car drivers who are keen about road safety and understand the requirement of decent driving on Indian streets.

Government Initiatives:

The Government of India also launched several initiatives for the expansion of the insurance telematics market. Some of them are given below:

- Union Budget 2021 increased the foreign direct investment (FDI) limit in insurance from 49% to 74%. India’s Insurance Regulatory and Development Authority (IRDAI) has declared that the digital insurance policies can be claimed through Digilocker.

- In June 2021, the government declared the extension of insurance coverage scheme worth Rs. 50 lakh (USD 66,850) for healthcare workers across India until the next year.

- In February 2021, it was announced by the Finance Ministry that Rs. 3,000 crore (USD 413.13 million) will be invested into state-owned general insurance companies for improvement of their overall financial health.

The future prospects are bright for the insurance telematics industry with many changes to be made in the country’s regulatory framework. This is projected to further change the way in which the industry conducts its business. The scope of IoT is likely to go beyond telematics and customer risk assessment. Currently, there are 110+ InsurTech start-ups in India. Moreover, demographic factors including young insurable people, rising middle class population and increasing awareness of the need for protection, and retirement planning are expected to support the growth of the Indian insurance telematics market in the coming years.

Author:

Karan Chechi

Research Director

TechSci Research

Mr. Chechi founded TechSci Research in 2009 with a mission to help people make informed decisions. The idea was to enable them to strategize with the lower risks and costs then they could perform better and set a benchmark in the market.

Mr. Chechi featured several times in leading newspapers and magazines and shared his viewpoint on several industry trends and educate people. He was honored with “Most Influential Market Research Professional” at Brand Excellence Awards organized by ABP News.

Published in Telematics Wire