COVID hits Shared Mobility

As the COVID-19 pandemic swept across the world, shared mobility startups along with almost all shared-economy businesses took a significant hit. As populations stayed home, mobility across the board ground to a halt and experienced adverse effects of the global lockdown. At the same time, this was also a time for many businesses offering mobility services to adapt to find viable solutions to adapt to the new market. All the companies started looking at providing value to meet the needs of a more conservative and cautious consumer market.

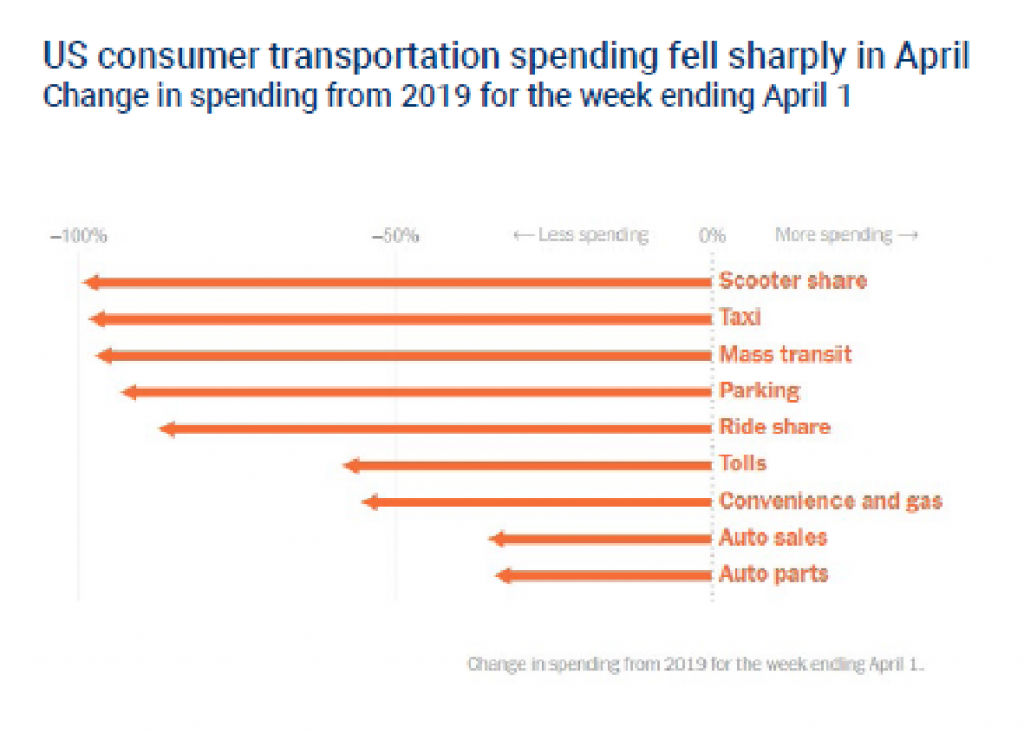

The statistics from US show the effect of the pandemic on the shared mobility ecosystem.

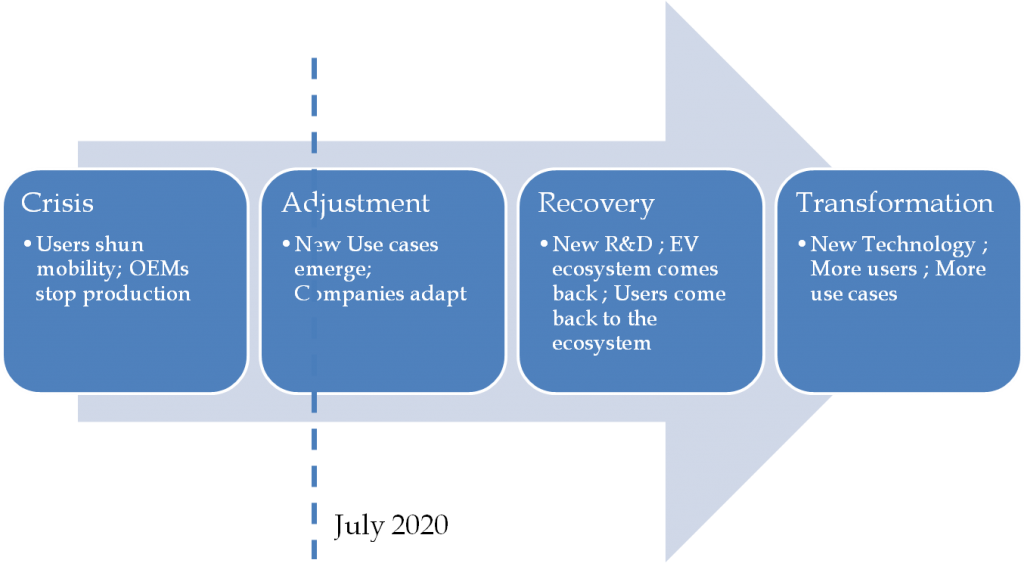

Stages of Shared Mobility recovery

The below pictures depicts the different stages towards the COVID revival and where we stand at the current context

We are in the ‘Adjustment phase’, where companies are adapting to the newer use cases of consumer behavior in the limited demand that’s picking up.

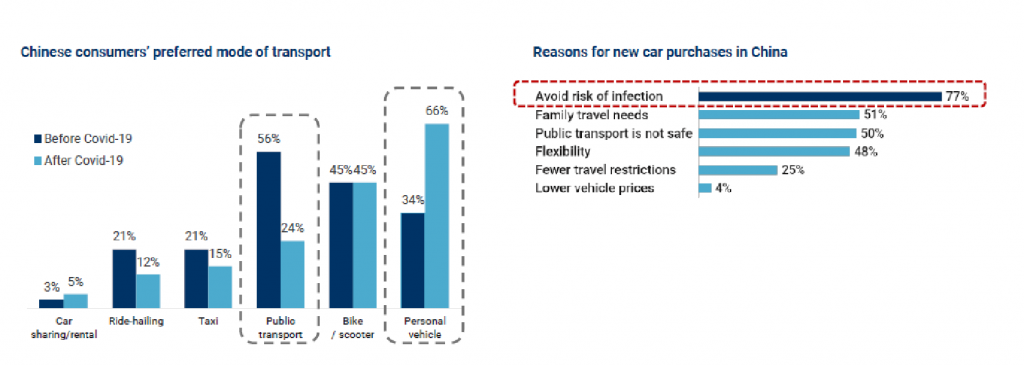

Some of the behavior changes can be seen from the below statistics from China

India Context

As markets reopened and partial restrictions were lifted, many commuters found themselves wary of using public transport. User trends are also showing a shift in preference to finding reliable personal mobility. There is evidence that the number of users who are attempting to solve their mobility needs by looking for two-wheelers have shown upward trends. At the same time they’re also seeking out more affordable ownership avenues like loans, and second-hand ownership. Yet the choices before most users seemed to be limited. As millions of people turned away from their previous dependence on alternative transportation modes, they were left with few choices:

- Two-wheeler ownership, which would tie them into hefty down-payments and EMIs, while also needing credit checks, documentation, maintenance, and taking on additional commitments including insurance and taxes. This isn’t ideal considering the limited financial stability many working professionals are experiencing during what experts agree is an economic downturn.

To expect individual consumers to take on more debt and long-term commitments while the market is dealing with job-losses and consumer spending in most areas has shrunk, makes the appeal of ownership an even more impractical solution for millions. - Second-hand/pre-owned vehicles already account for a large volume of use today, but happen largely with cash-based transactions and operate with a persistent need for the buyer to evaluate the quality of vehicles before being purchased.

Even in this scenario, any consumer today would be hard pressed to have the immediate liquidity needed to purchase the vehicle, but also the added maintenance costs involved with a used vehicle. - Ride-sharing and bike taxi services will also be challenging because they’re inherently exposing users into contact with strangers which they would ideally like to avoid. Plus, since these services still haven’t reached critical mass, and are still mostly unpredictable, they also cannot be expected to scale to meet the demands of mass mobility like private two-wheelers are able to solve.

COVID Driven Use cases

Towards the new use cases, technology companies have started offering the new services such as

Hourly / Daily Bookings: The most popular service that mimics the initial use-case of most users who use shared mobility intermittently,

Monthly Subscriptions: Service to solve mobility for everyday needs for extended periods of time

These plans allow users to experience the same joys of ownership without the added costs of insurance, maintenance, and hefty payments while also offering them the advantages of switching to another bike as per their needs or even flexibly changing their plans to suit the extent of their anticipated use.

This plan was growing in popularity until the lockdown began but has gradually begun picking up again as offices reopen and users are cautiously pick up plans to meet their requirements without getting straddled with down-payments and insurance/maintenance costs

Rent-to-Own: Rent-to-own plan allows users to pick from any of the existing bikes, but without the hassles of extensive documentation, credit checks or even any down-payments. Anyone can almost instantly pick-up any scooter/motorcycle of their choosing and rent it monthly for a chosen term, at the end of which the vehicle ownership is transferred to the user. Plans typically offer either a 12 or 18-month term, allowing users to rent today and own tomorrow.

Surging demand for ecommerce and delivery

Companies are repurposing their fleets to take care of the surge in demand for home delivery of essentials and other products.

Technology Levers

Electrification, Battery Infrastructure

Falling battery costs and lower maintenance costs will spur the adoption in the recovery phase’ This will be further propelled by the interest from larger corporations and energy, oil companies as they prepare for the future ahead with EV.

Connectivity

Connectivity technology will drive use cases around hardware connectivity, personal connectivity, safety, individual preferences and personalisations

Autonomous

While self driving technology requires higher investment, there will be different use cases that will drive the demand of this technology

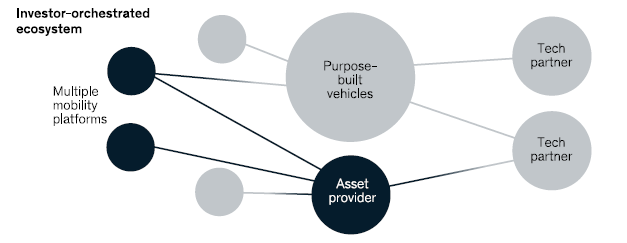

It is envisaged that the ecosystem will grow based on collaborations across mobility platforms providers, OEMs, technology providers, Asset providers.

Future Ahead – Shared Mobility for 2 Wheeler

A number of startups are working on shared vehicle networks, vehicle design, and charging infrastructure for bicycles, scooters, mopeds, and other compact vehicles apart from them trying to take the advantage of the whole EV technology benefits.

As per World Bank data, 850 million of Indian are below the age of 35 and since young people are usually quicker to adopt new trends and are less likely to own a car, implying a likelihood of adopting new mobility options.

By 2030, Morgan Stanley expects shared miles to reach 35 per cent of all the miles travelled in India and this will further increase to 50 per cent by 2040.

Post 2030, it also expects this trend of shared mobility to partly replace individual car ownership while app-based taxi services will mainly replace public transport rather than personal car usage. India had 257 billion miles driven in 2017, and of that, 10 per cent were shared (includes traditional taxis and app-based plays), and it is believed that it can rise to 35 percent by 2030 implying 18 percent CAGR based on Morgan Stanley estimates.

While there is lot of negativity is around the shared mobility sector, but the critical analysis of the data suggests that the future ahead for the shared mobility startups is rosy.

Published in Telematics Wire